The US consumer: mixed signals

The corporate world’s top customer has remained in rude health this year.

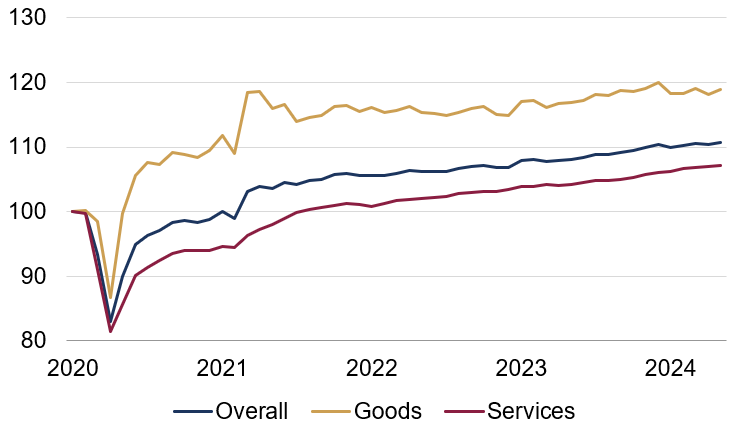

US consumer spending, which accounts for roughly two-thirds of domestic GDP, has continued to rise in real terms through the first half of 2024 (figure 1). Yet, there are (again) growing concerns that it could slow – or even reverse – from here, amid lower household savings, subdued confidence and rising loan delinquency rates.

Is consumer momentum set to falter, or are there tailwinds that may offset the above risks?

Figure 1: Monthly US personal consumption expenditures

Rebased indices (real terms, Jan 2020 = 100)

Source: Rothschild & Co, Bloomberg

Lower savings and confidence…

Many things shape consumer spending, but it helps to group them into two main variables: things which affect household income, and things which affect the proportion of that income which is spent.

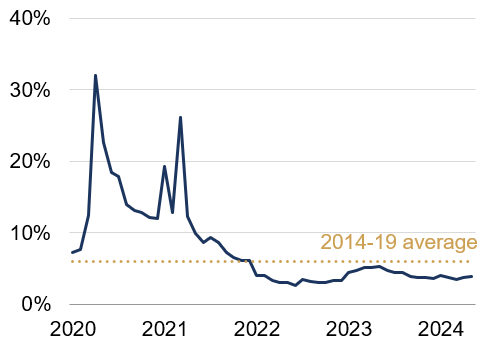

Taking the latter first, US households have been spending a bigger proportion of their disposable income of late. But with spending running above its pre-pandemic rates now for two-and-a-half years, the US consumer may be running out of room on this account. The flip side of a higher spending rate is a lower saving rate (figure 2).

How much of their income is spent or saved may depend on how confident consumers feel about their employment, incomes and wealth, and to some extent on the level of interest rates (which can increase the incentive to save). Consumer confidence surveys have indeed declined over the past few months. Although, we would not place much emphasis on these surveys: they are not closely correlated to actual spending, and responses can be heavily distorted by political affiliation (see here).

Figure 2: US household savings rate

(%)

Source: Rothschild & Co, Bloomberg

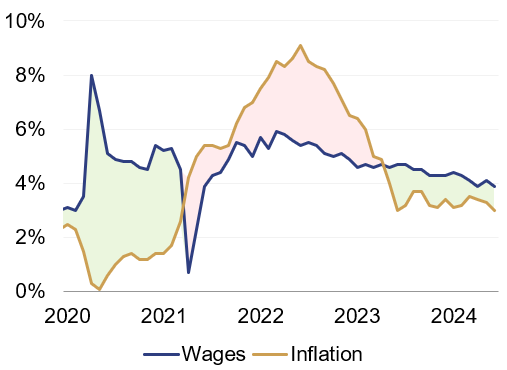

Figure 3: Real wage growth

Year-over-year (%)

Source: Rothschild & Co, Bloomberg

... but real incomes are growing again

However, households’ disposable incomes, which were hurt by the initial rise in inflation, have been growing again for almost two years in inflation-adjusted terms. Along with the elevated spending rate, this explains the more recent resilience in consumer spending, and if real incomes accelerate, households may even be able to rebuild their savings rate while maintaining their levels of spending.

We think wages will continue to grow faster than inflation through the rest of this year (figure 3), which will offer some support to disposable incomes and spending, even if weaker confidence does begin to make itself felt.

Interest rates are having some impact…

Higher interest rates affect the proportion of income which is spent, as noted – whether by directly increasing the incentive to save, or by affecting the value of savings, through ‘wealth effects’ (such wealth effects do not always materialise as interest rates go up: recently, for example, bonds have been weak, but stock prices have actually risen).

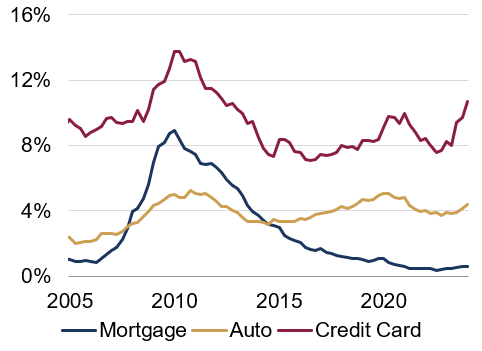

But for hard-pressed consumers with big loans, higher interest rates can hit disposable incomes directly. In this cycle, distress has been most visible instead in auto and credit card loans. The proportion of borrowers that are in the ‘serious’ delinquency category here – a sign of economic distress – has risen markedly, though is still below Global Financial Crisis highs (figure 4).

That said, non-mortgage credit is relatively small, and matters most to low-income households, and less to those on higher incomes. The bottom-quintile income group contributed less than 10% of total US consumption expenditures in 2022, compared to a figure closer to 40% for the top-quintile income cohort. As a result, higher auto and credit card delinquency rates may not hit total consumer spending as hard as one might think.

Figure 4: Aggregate delinquency rates 90+ days delinquent

(% of balance)

Source: Rothschild & Co, Federal Reserve Bank of New York

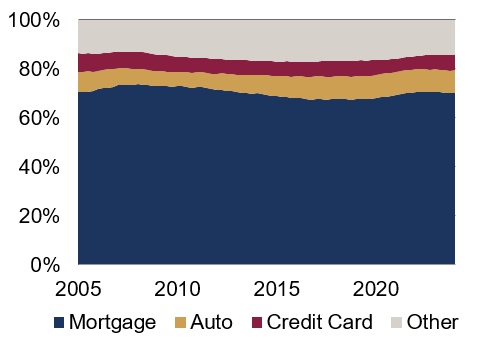

Figure 5: US household debt

(% of total)

Source: Rothschild & Co, Federal Reserve Bank of New York

… but mortgage delinquencies remain low (and matter most)

Importantly, mortgage delinquency rates have remained near multi-decade lows (figure 4, again). US households typically have 30-year fixed-rate mortgages, and so are largely insulated from higher interest rates. The effective rate on all outstanding mortgages is still just 4%, a few percentage points below the rate a household would pay if they were to move home today. Moreover, borrower creditworthiness is higher nowadays and almost 40% of US households own their home outright.

Mortgages make up about 70% of US total household debt, and so the bulk of most households’ outgoing payments are in fact shielded from higher interest rates (figure 5). Auto and credit card loans only account for 15% of total household debt, and as noted, are a bigger share of lower income households’ liabilities.

We think mortgage delinquency rates are likely to stay low, unless unemployment rates rise significantly (which is not our central case). And with US interest rates set to fall from here, the strain on even low-income households may gradually abate. Clearly, the impact on spending power from higher interest rates is more nuanced than economic textbooks suggest.

Verdict: Consumer spending can continue to grow

Overall, we still give the US consumer the benefit of the doubt. Ongoing real wage growth can sustain spending, while interest rates have not affected households in a uniform manner (and may decline from September). Labour market developments are of course crucial to both confidence and incomes, but they remain healthy for now.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

The Sick Man of Europe

Strategy Blog

Germany’s economy shrank in the second quarter – and is currently little bigger than it was in 2019. Two big negative supply shocks will have played a major part, but is something more fundamental at play? In this strategy blog we explore the reasons why.

-

Serious, not hopeless

Market Perspective

Global temperatures are rising. In this Market Perspective we reflect on some of the long-term economic questions raised by climate change. We examine its recent inflationary effect and some of the practical issues we encounter when trying to invest sustainably.

-

Have markets settled down?

Perspectives podcast

Historically, August and September have been weaker months for U.S. stock returns. However, last week’s global market sell-off took investors by surprise. How should we interpret these events, and what do they mean for our strategies?

-

Asset Management: Monthly Macro Insights - August 2024

Market Commentary

Weakening business confidence indices continue to cast doubts on the global economy’s resilience. Although core inflation remains above central banks’ targets, the cooling of labour markets has not gone unnoticed, prompting a major shift in policy rates projections.

-

Growth Equity Update

Insights

The August edition assesses the recent strength of the European VC market. With July also being a strong month for IPOs, with $5.5bn raised in the US. We do a deep dive on LegalTech following a recent spate of VC raises. Plus, we look at the likelihood of the Fed cutting rates in September and the possible market reaction.

-

The AI trade loses some steam

Monthly Market Summary

Global equities moved higher by 1.6% in July (USD terms), while global government bonds returned 1.8% (USD, hedged terms).