Five stock market talking points

Stocks have continued their ascent during the first half of this year. The MSCI All Country World Index (ACWI) – the global benchmark – has returned 11% so far in US dollar terms, hitting another all-time high in June (however, the index is still 7% below its late-2021 inflation-adjusted high).

Just as we did last year, below we flag five striking observations from stock markets at the halfway point of 2024.

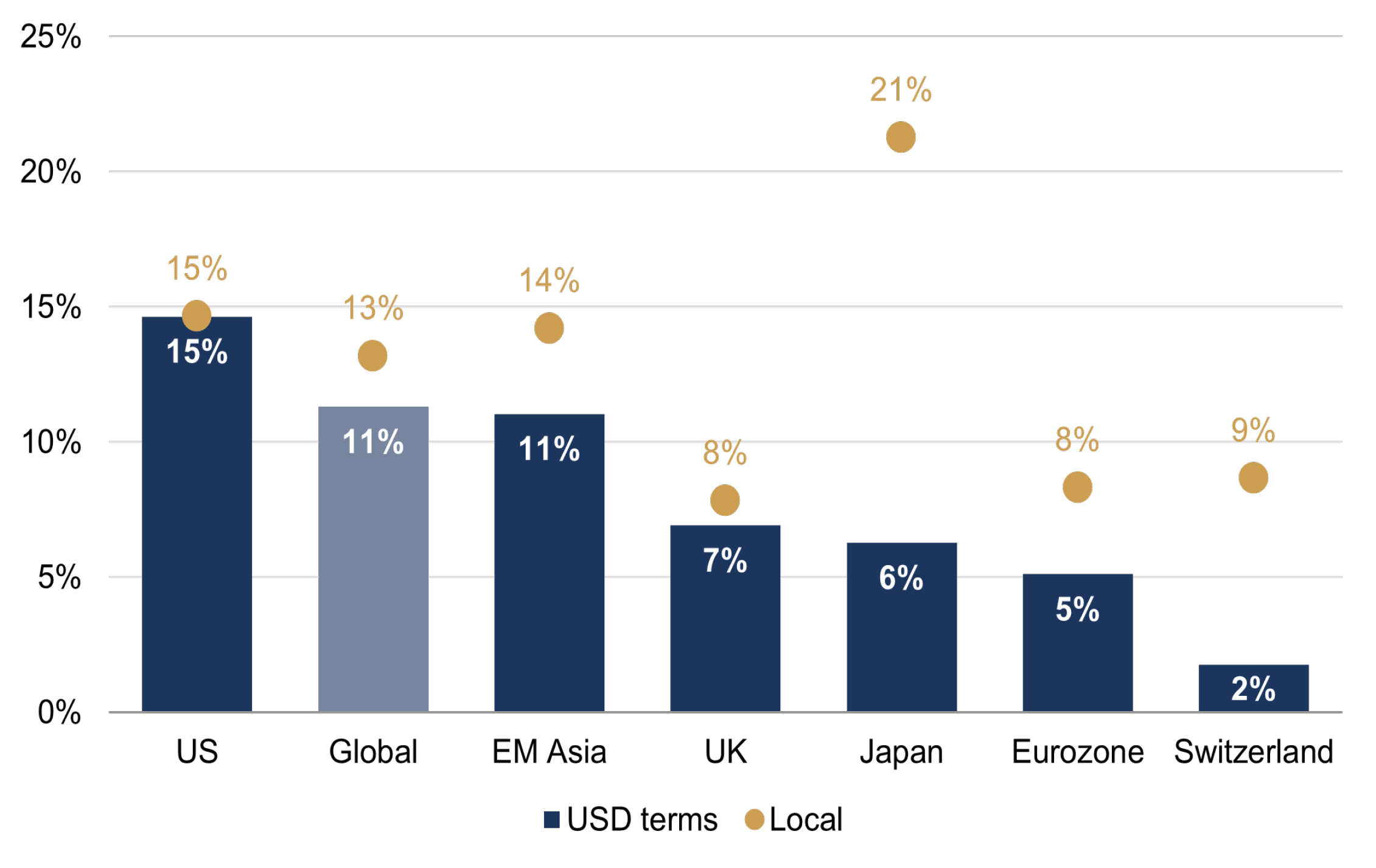

1. Ongoing US exceptionalism…

The US has outperformed the global benchmark this year in common currency terms, and it now accounts for almost two-thirds of that index. ‘Growth’ and ‘cyclical’ style stocks have outperformed ‘value’ and ‘defensives’ this year (respectively), and the US of course has a higher weighting in technology (and other ‘growth’ style sectors). There have been healthy local currency gains in some other regions, but the stronger dollar has reduced their value to unhedged global investors. In the case of Japan, the yen’s collapse has translated a striking local currency gain of 21% into a USD return of just 6%.

Figure 1: Year-to-date ranked returns by region (%)

Source: Rothschild & Co, Bloomberg, MSCI

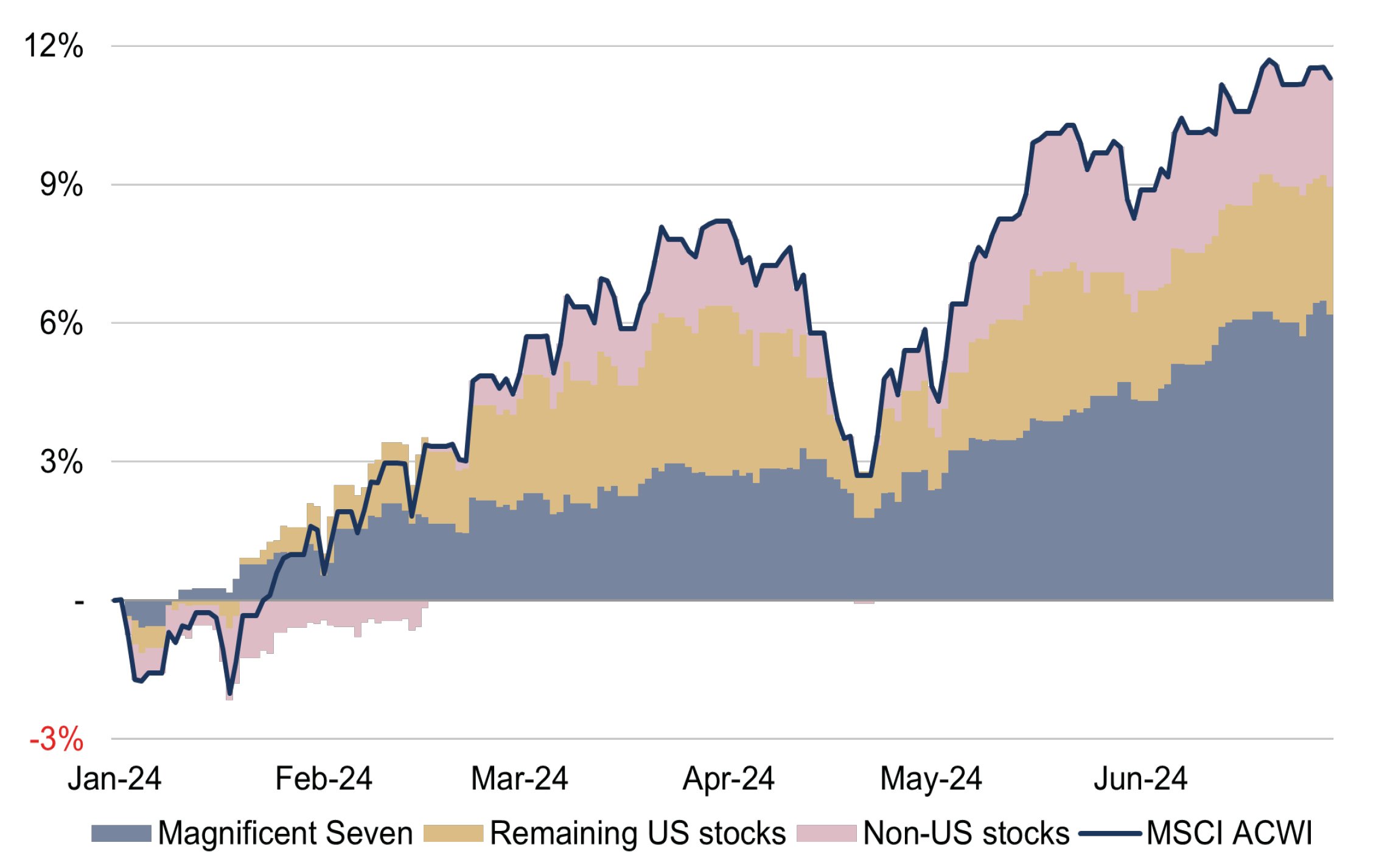

2. …driven by a handful of (AI-related) stocks

Global stock market leadership has remained narrow this year, with the US mega-cap ‘Magnificent Seven’ cohort – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla – reaping the rewards from ongoing AI-related momentum, albeit in a more fragmented manner (Tesla has bucked the trend and is down by a fifth this year). The Magnificent Seven have accounted for more than half of the MSCI ACWI’s 11% year-to-date return – roughly a quarter of global returns have been driven by Nvidia alone – and almost all of its second-quarter returns. Conversely, the equal-weighted US index was only up 5%, and US small caps’ returns were just 2% in 2024.

Figure 2: Year-to-date global stock market contributions (%pts, USD)

Source: Rothschild & Co, Bloomberg, MSCI

Note: Magnificent Seven consists of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

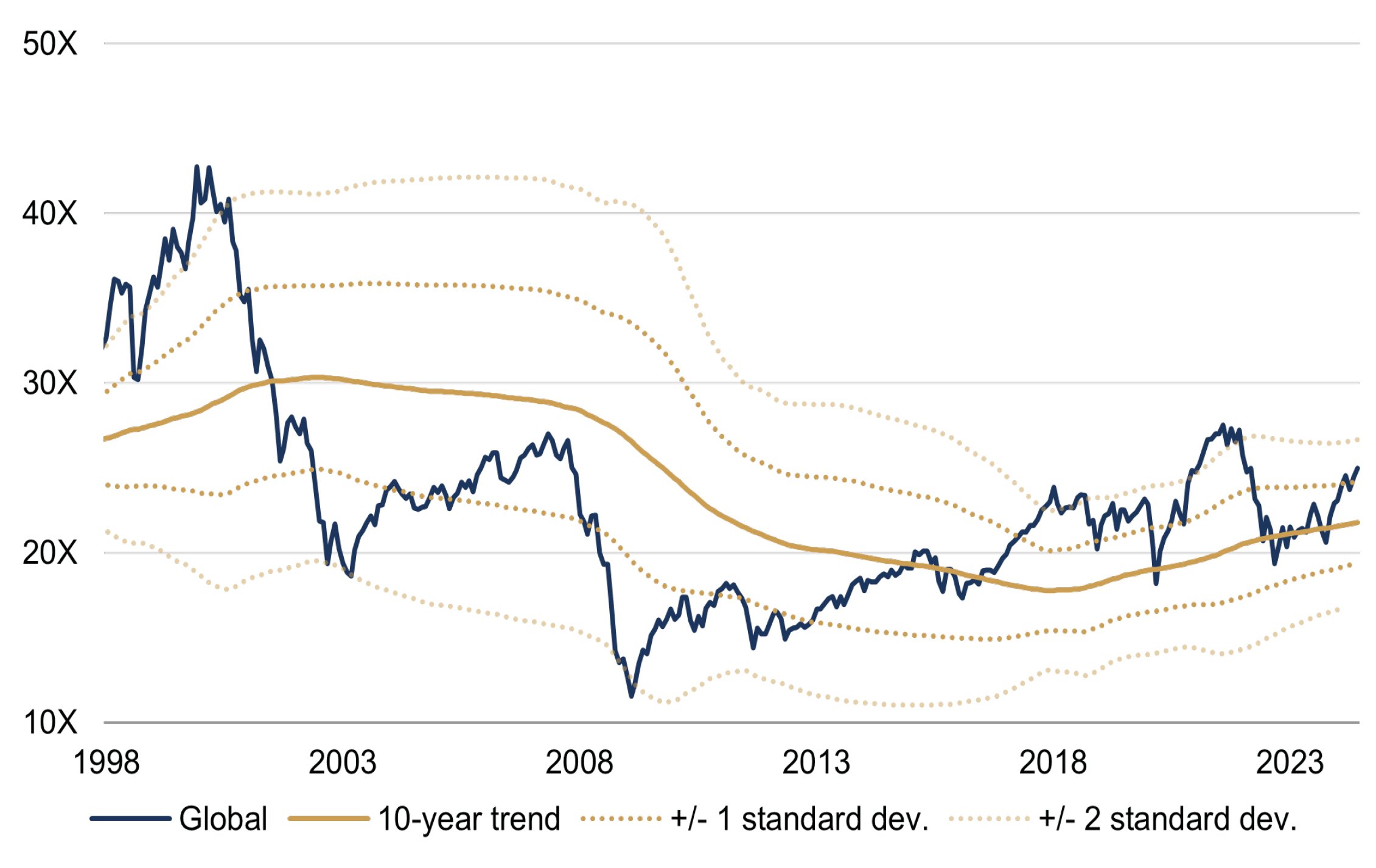

3. Not a frothy market (for now)

Global stocks have also become dearer this year. Our preferred long-term valuation metric, the cyclically-adjusted price-earnings (CAPE) ratio – the inflation-adjusted price relative to the inflation-adjusted 10-year moving average in trailing earnings – has risen to more than one standard deviation above its long-term trend. However, this is not alarmingly expensive. During the dot-com bubble, the global CAPE was more than two standard deviations above that trend and trading at over 40X, versus 25X today. While we don’t use valuations as a short-term timing tool, they can matter more when near extreme highs and lows – but that is not the case today.

Figure 3: Global stock market valuations (cyclically-adjusted price-earnings ratio, X)

Source: Rothschild & Co, Bloomberg, Datastream, MSCI

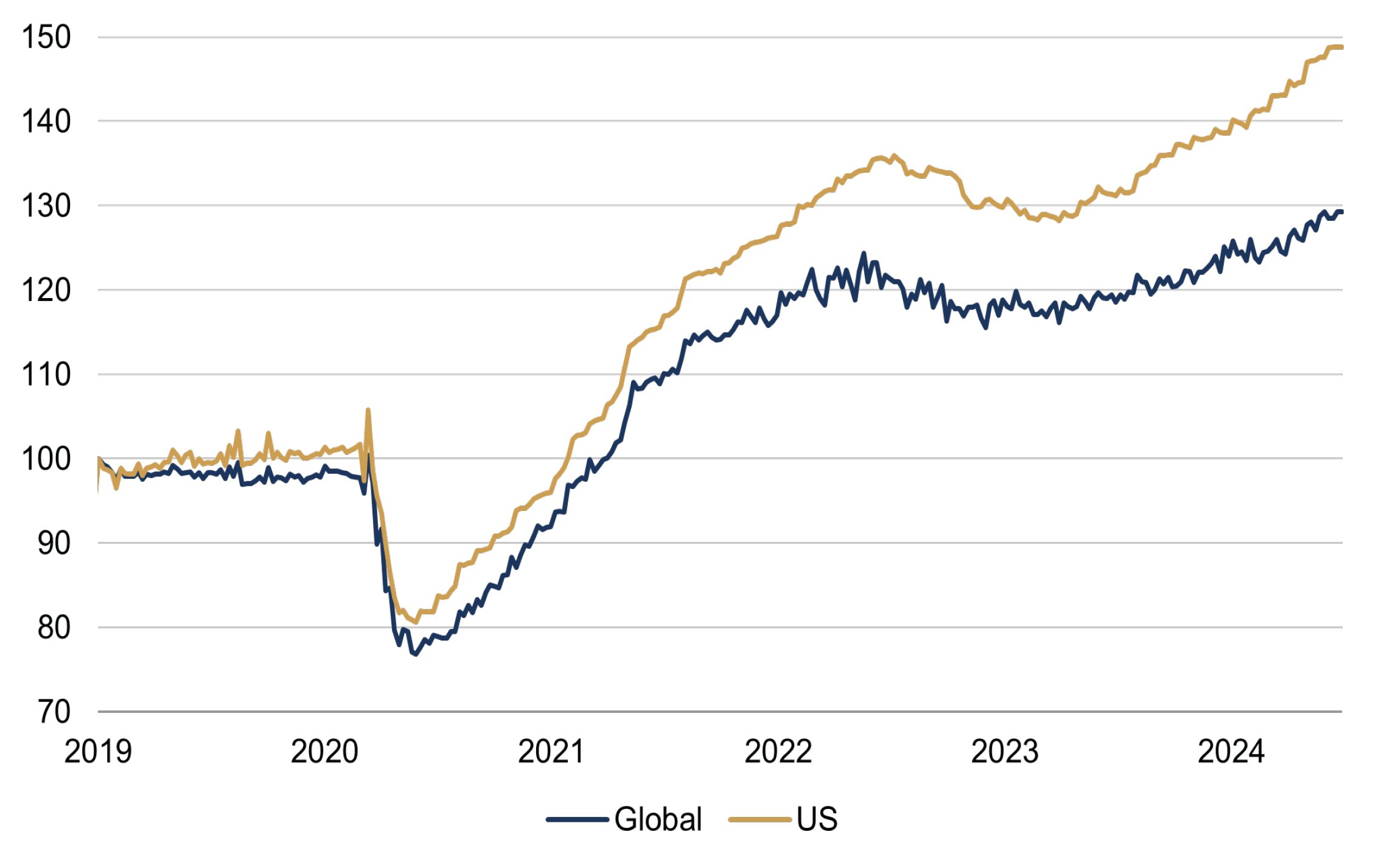

4. Corporate earnings (and expectations) have turned a corner

Global earnings stagnated in 2023, meaning the last year’s stock market rebound was driven primarily by those rising valuations. Promisingly, trailing – or actual – earnings appeared to tentatively pick up towards the end of last year, most notably in the US, where there have been a few quarters of positive earnings growth. Admittedly, this has mostly been due to strong profits at some of the mega-cap names in the Magnificent Seven, but analysts are expecting earnings to broaden across other sectors this year, which is plausible given ongoing economic resilience.

Figure 4: Forward earnings expectations (12-month forward earnings per share, rebased to January 2019)

Source: Rothschild & Co, Datastream, MSCI, I/B/E/S

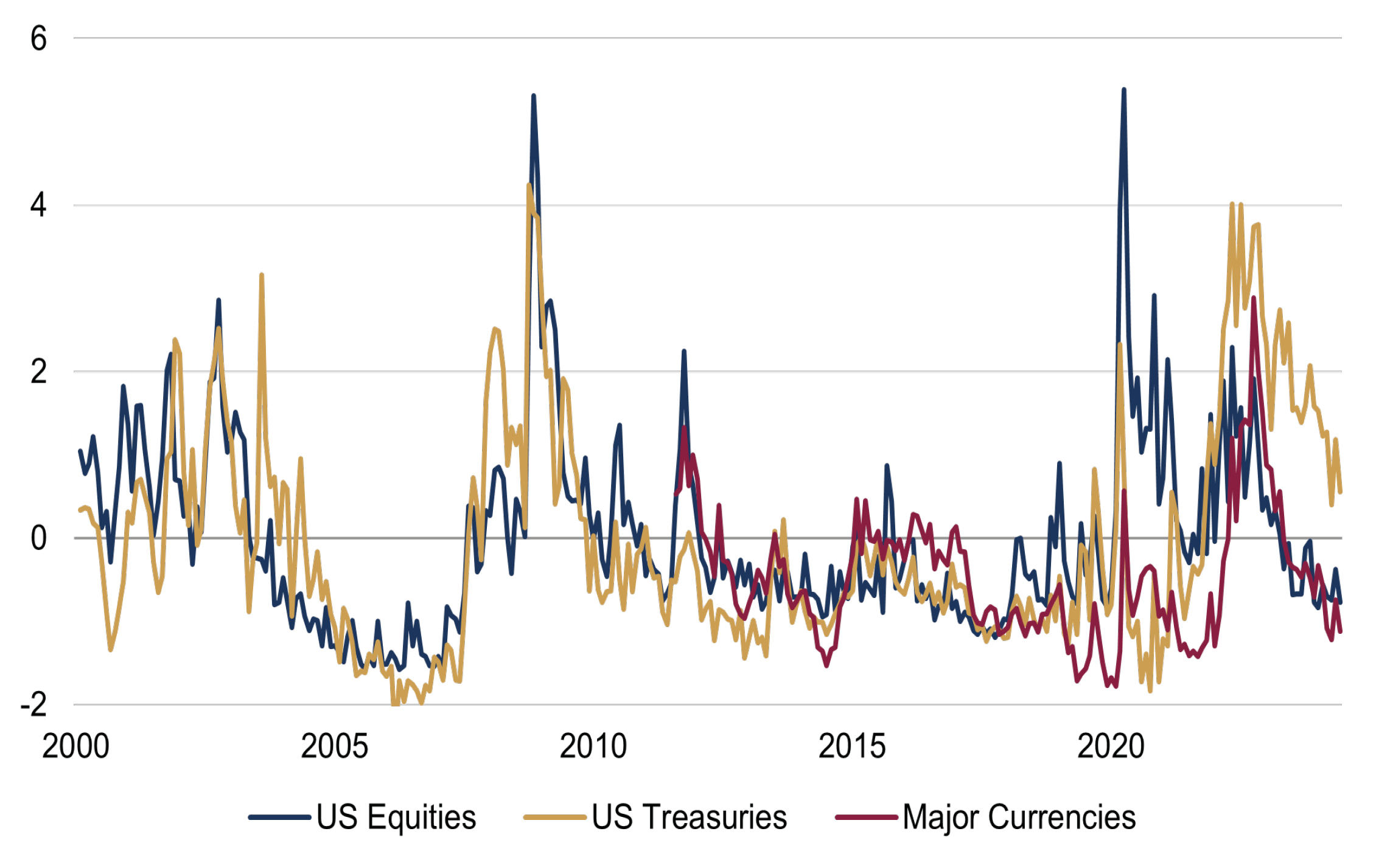

5. Volatility remains unusually subdued

Stock market volatility has remained remarkably low this year. There has only been one trading day in 2024 where the S&P 500's daily price change has been greater than 2% (in absolute terms), following just two days in 2023 (compared to 46 trading days in 2022). In fact, global stocks have moved higher in a linear fashion since the end of October, aside from a brief sell-off in April. Moreover, from a cross-asset perspective, it is very unusual for implied volatility – derived from the prices of derivatives, or portfolio insurance – to be lower than normal for stocks, yet higher on average for bonds. It would not be surprising if stock volatility picks up from here, particularly given the busy political calendar, but for long-term investors it is the wider business cycle that matters more – and there are few signs of a downturn looming.

Figure 5: Cross-asset implied volatility (z-scores, normalised)

Source: Rothschild & Co, Bloomberg

All charts and data as of 30 June 2024.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

French election: first-round outcome

Strategy Blog

In this strategy blog, we look at the first-round of the French election, and how local markets could be affected by the final verdict.

-

Macro update: polls, populists, policy and portfolios

Strategy Blog

In this strategy blog, we look at how polls, populists, policies and portfolios are affected by recent, and upcoming macro events.

-

Our culture, service and people

Insights

We pride ourselves on our company culture, values and people at Rothschild & Co Wealth Management UK. Our business is built on the strength of our people and the relationships they have with clients, and we believe this sets us apart from other wealth managers.

-

Sportonomics and the winners away from the arena

Thematic Insights

The Olympic motto 'citius, altius, fortius' - faster, higher, stronger - reflects the sport industry's rapid evolution. Younger generations are redefining their engagement with athletes and sports, driven by new technologies.

-

Making the best investment choices

Insights

There are many ways you can grow and preserve your wealth by investing. In this article we discuss how to find an investment style that suits your outlook, examine both ‘top-down’ or ‘bottom-up’ investing strategies, and assess active and passive investing.