Global manufacturing revival?

The US ISM manufacturing survey, one of the longest-lived cyclical indicators, disappointed for the third consecutive month in June. However, the wider global picture looks rosier.

The S&P Global Purchasing Managers' Indices (PMIs) track manufacturing sector developments across countries. Thousands of firms are surveyed each month, and in more than 40 nations, accounting for 98% of global manufacturing value added. Firms are asked if business conditions have improved, deteriorated, or remained unchanged: a neutral – or ‘no change’ – reading corresponds to 50, while figures above (or below) this threshold indicate expansion (or contraction). Importantly, the PMI data tend to fluctuate around a constant mean, identifying turning points in the manufacturing cycle, with ‘no change’ in practice corresponding to trend economic growth.

In this dataset, US manufacturing has in fact been expansionary throughout this year, and other regions’ data seem to have also improved (figure 1). Several factors may explain the divergence between the ISM and S&P Global series, including industry coverage, company size (the ISM focuses more on large companies), geographical coverage (the S&P Global survey focuses on US operations only), sample size, methodology (seasonal adjustments) and component weightings.

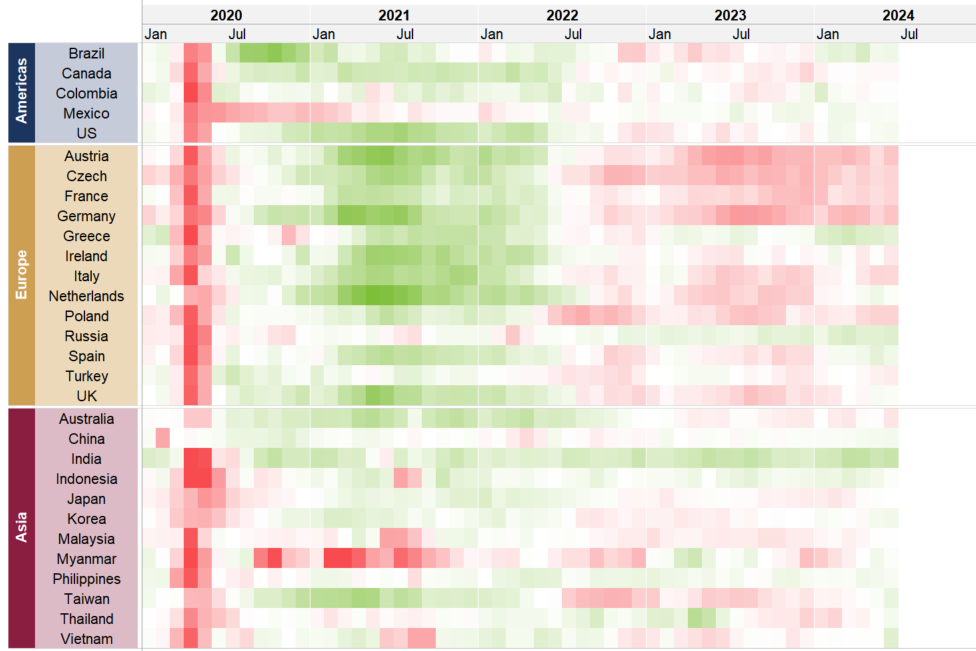

Figure 1: Manufacturing PMI heatmap

(Diffusion indices, 50 = “no change”)

Source: Rothschild & Co, Bloomberg, S&P Global

Note: The manufacturing PMI ranges from 0 to 100, with a reading of 50 indicating 'no change'. A (green) reading above 50 is expansionary, while a (red) reading below 50 is contractionary. The further away from 50 the greater the change.

Regionally, European manufacturing has generally remained weak, particularly in those countries that were more dependent on Russian gas, such as Austria, Germany and the eastern European economies. Still, it’s possible that manufacturing activity may recover even in those nations, as they slowly transition away from Russian gas (wholesale natural gas prices have of course collapsed by 90% from their 2022 high), and may also benefit from the gradual decline in interest rates.

Meanwhile, almost all June S&P Global PMIs were in expansion territory in the Americas and Asia, with the most visible improvements occurring in the latter region. In recent decades, China and the surrounding EM Asia countries have played an increasingly pivotal role in global trade – low-income nations tend to produce the more basic goods, while countries such as Taiwan produce most of the world’s high-quality semiconductors – and developments there may provide early clues on the direction of the global manufacturing cycle.

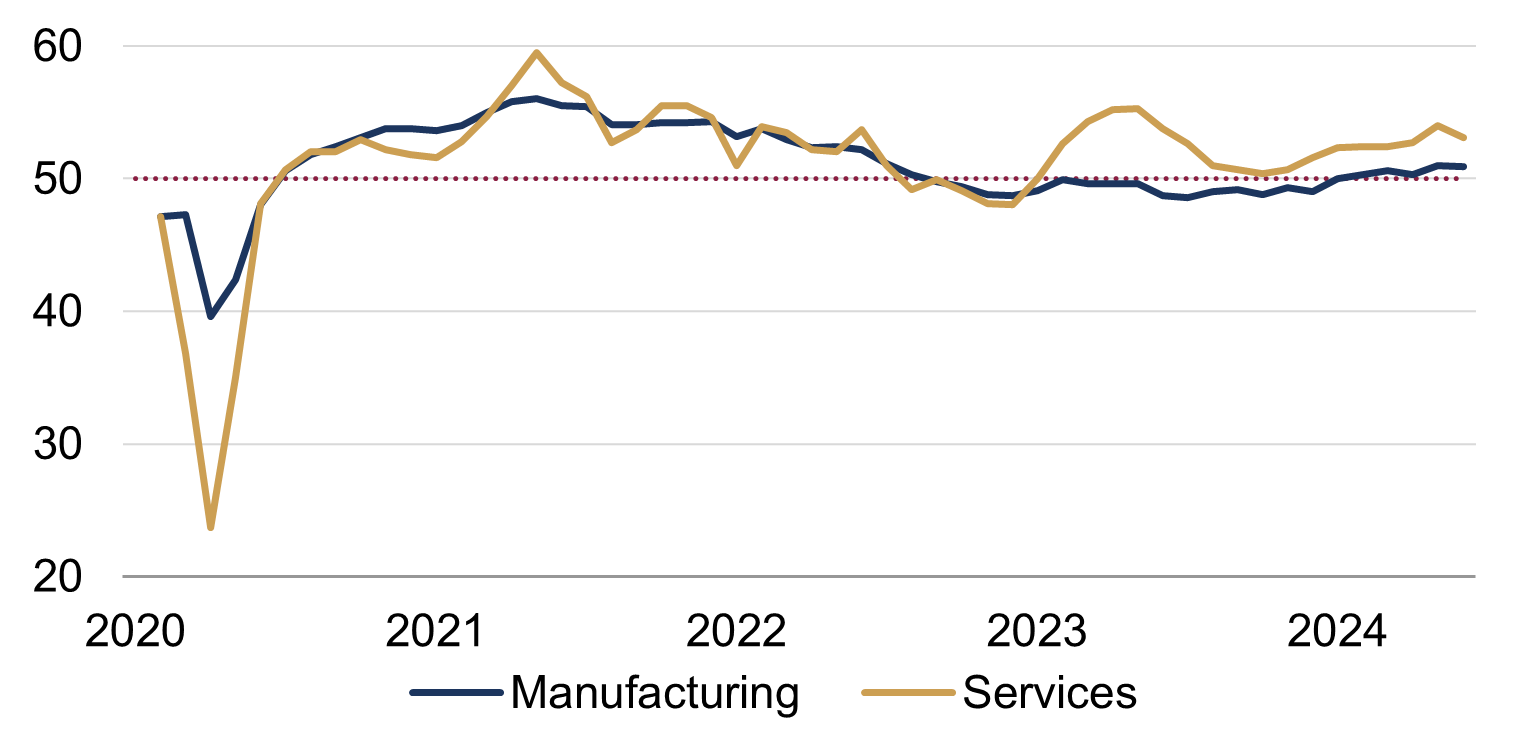

Of course, the services economy accounts for a greater share of global GDP nowadays, but it has also been robust over the past couple of years. Currently, the S&P Global PMIs suggest that both global services and manufacturing are in ‘expansion’ territory (figure 2). If accurate, this suggests that the resilience in corporate profitability may persist into H2.

Figure 2: Global manufacturing and services PMIs

(Diffusion indices, 50 = “no change”)

Source: Rothschild & Co, Bloomberg, S&P Global, J.P. Morgan

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

The US consumer: mixed signals

Strategy Blog

Should we give US consumer spending the benefit of the doubt? Real wage growth has continued while rising interest rates have not affected all households in a consistent way. In this strategy blog we take a look at the health of the US consumer market.

-

The perils of making predictions

Quarterly Letter

History is littered with examples of people making predictions that later turned out to be inaccurate. How can we become better at forecasting the future? Our Quarterly Letter delves into this topic to investigate some of the perils of making predictions.

-

Rothschild & Co’s UK Wealth Management business names James Morrell as Deputy CEO

Press releases

The newly created Deputy CEO role will provide increased capacity at a senior level to help meet the growing demand for Rothschild & Co’s wealth management services from existing and future clients.

-

Rothschild & Co wins Western Europe's Best Bank for Advisory from Euromoney

Awards

This is the second consecutive year we have been named Western Europe's Best Bank for Advisory, reflecting the breadth of our capabilities across M&A and financing advisory across the region.

-

Is small beautiful again?

Strategy Blog

Large companies have typically offered far more attractive returns than their smaller counterparts, but that has changed recently. What’s behind the reversal? In this strategy blog we examine the reasons behind the switch and whether this trend is likely to continue.

-

A mid-year review with our CIO and Global Investment Strategist

Perspectives podcast

A mid-year review on the main macroeconomic developments and how our strategies have perfomed with our CIO Dr. Carlos Mejia and Global Investment Strategist Kevin Gardiner.