Is small beautiful again?

In a dramatic reversal, small US stocks have been beating big ones recently. Last Thursday, the Russell 2000 index (average market cap approximately $1 billion) jumped by 3.6% in a single day. It is now up by 8.3% since 9 July, while the S&P500 (average market cap around $100 billion) is down slightly since then.

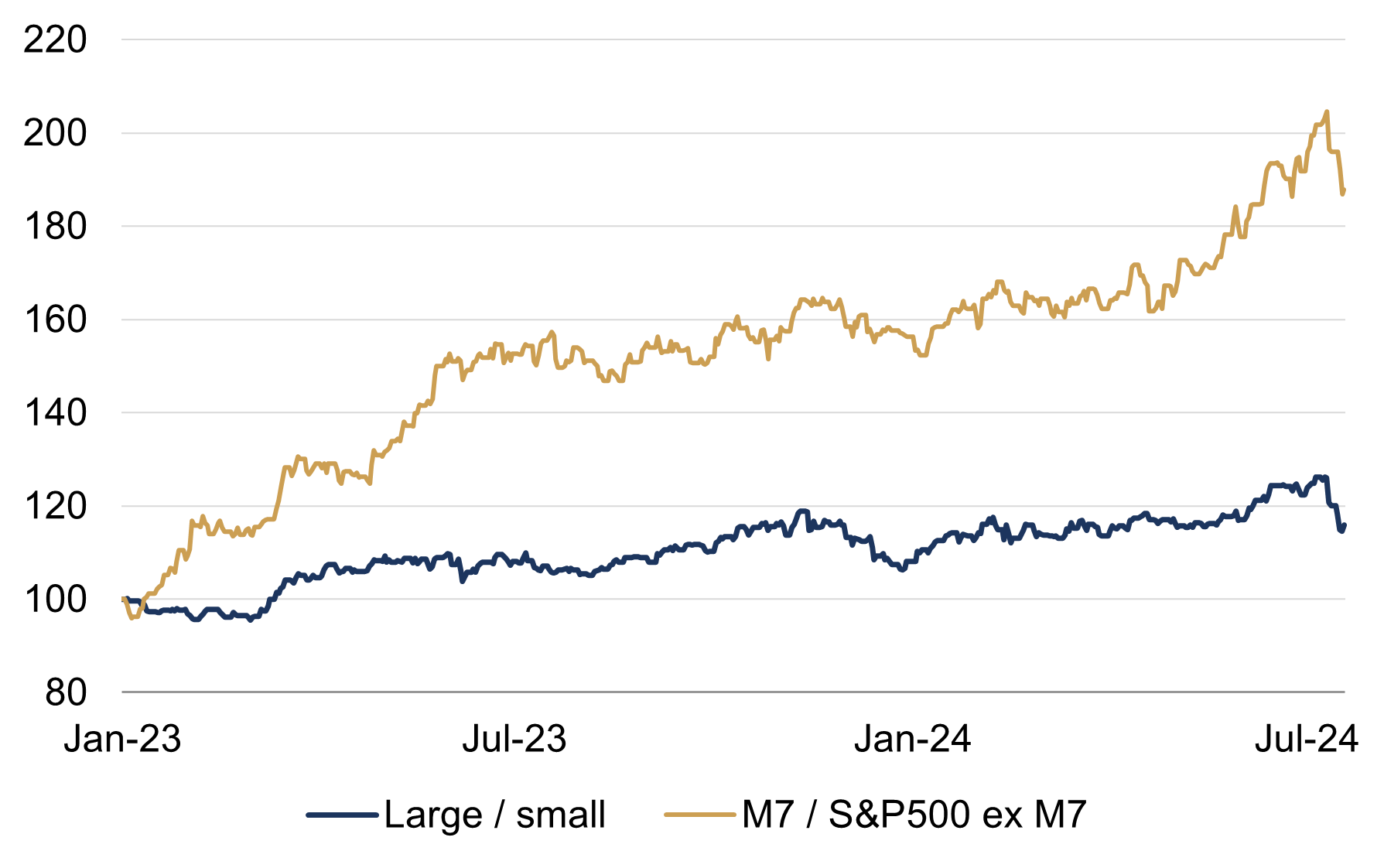

The reversal has coincided with a sell-off in the ‘Magnificent Seven’ mega caps, whose surge since the start of 2023 has made the US (and global) market’s ascent so narrowly-based (figure 1).

Figure 1: Relative stock market returns

Rebased indices (Jan 2023 = 100)

Source: Rothschild & Co, Bloomberg

Note: Large vs small is the S&P500 index relative to the Russell 2000 index.

So, is the ‘small company effect’ back? Is this the beginning of the long-awaited broadening and rotation of market leadership more generally?

The idea that smaller companies tend to outperform bigger ones over the long term is part of market folklore. Two US academics, Fama and French, identified it as one of the factors in their influential ‘three factor model’ of investing (Multifactor Explanations of Asset Pricing Anomalies, Journal of Finance, March 1996).

The idea that broad is best when it comes to market leadership is also deep-seated, though it has no academic pedigree. As macro analysts we have been relatively relaxed about the recent narrowness (see here), but we’d still be happier if market gains had been broader.

The trigger for the reversal seems to have partly been related to an escalation in protectionist rhetoric around the global semiconductor industry. This perhaps encouraged some profit-taking in the tech-led Magnificent Seven trade, and a search for more conventionally cyclical stocks, as another good US CPI release confirmed that lower interest rates were looming closer. Small companies had lagged for some time, leaving their stock valuations way below those on the more fashionable Magnificent Seven bloc, and they are typically more exposed to the business cycle.

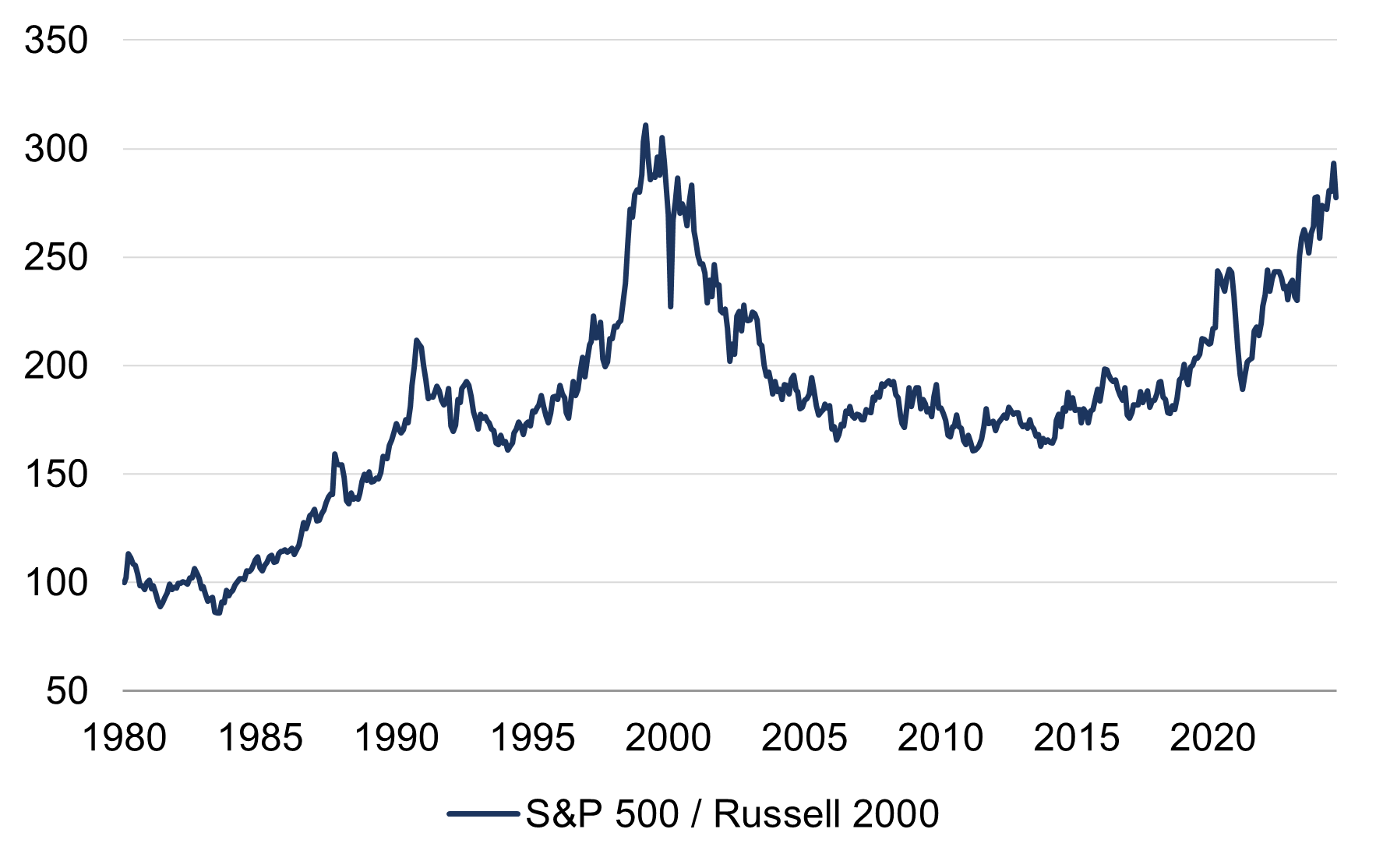

Figure 2: Relative stock market returns over the longer run

Rebased index (Jan 1980 = 100)

Source: Rothschild & Co, Bloomberg

However, as figure 2 makes clear, the recent reversal retraces a tiny portion only of an underperformance dating back to 1980. It is clearly way too soon to proclaim a major turning point.

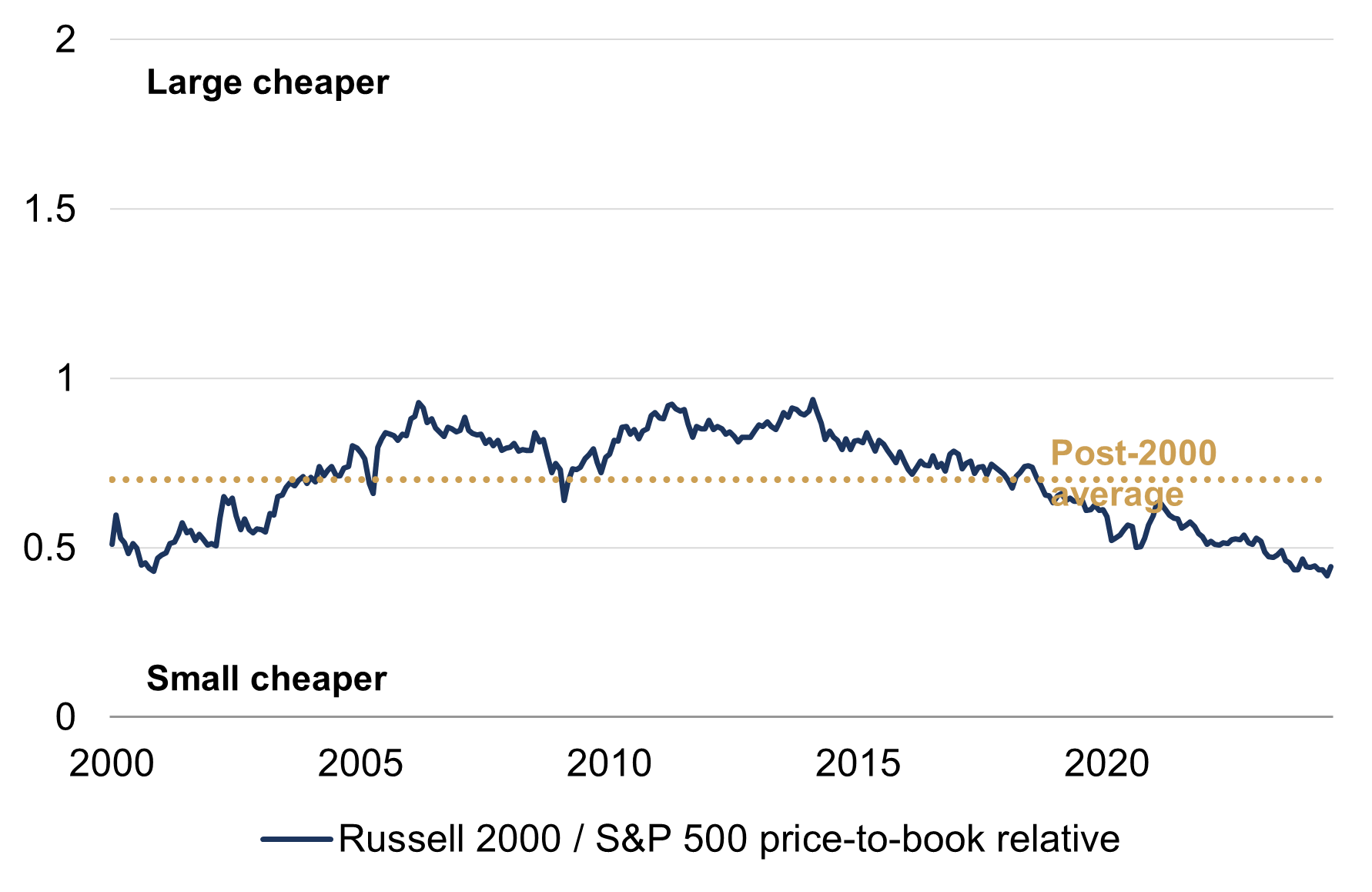

Figure 3 shows that the small cap index is certainly significantly cheaper now: its relative price-to book ratio has lagged far behind the S&P500’s, and indeed has not risen in absolute terms since the 1990s. But cheapness alone is clearly no guide to short-term returns: why might it suddenly matter now, when it didn’t when relative valuations were already low in (e.g.) 2019?

Figure 3: Relative price-to-book ratio

Source: Rothschild & Co, Bloomberg

Arguably, figure 2 in fact suggests that any systematic ‘small company effect’ had perhaps evaporated even before Fama and French published their paper.* Small may never have been truly beautiful in the investment context.

It is not clear why such a thing should exist to begin with.** Size itself is surely a less important driver of business success than the product, the nature of the business itself. Even the largest company can remain competitive, while many small companies are small for a reason.

This doesn’t mean that small companies are not well placed now. Falling interest rates and domestically-oriented consumer-led growth should indeed be helpful for businesses with weaker balance sheets and insufficient scale to go global, and as noted they look inexpensive. They can do well alongside other sectors. But it is too soon to say that they are poised to take a lasting lead – it is similarly too soon to call time on the Magnificent Seven leadership, even if we’d like to – and there may be no reason for thinking that they should.

* While we’re on the subject, there is little evidence elsewhere of stable betas, or of the outperformance of value, two of the other factors in that ‘three factor model’. We will return to the usefulness of much finance theory in a future post.

** Belief in such a thing extends beyond stock market analysis. It has been suggested that some regional economies here in the UK haven’t grown faster because of the lack of SME-sized enterprises. It can just as easily be argued that there are fewer SME-sized enterprises because we haven’t grown faster.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

The US consumer: mixed signals

Strategy Blog

Should we give US consumer spending the benefit of the doubt? Real wage growth has continued while rising interest rates have not affected all households in a consistent way. In this strategy blog we take a look at the health of the US consumer market.

-

The perils of making predictions

Quarterly Letter

History is littered with examples of people making predictions that later turned out to be inaccurate. How can we become better at forecasting the future? Our Quarterly Letter delves into this topic to investigate some of the perils of making predictions.

-

Rothschild & Co’s UK Wealth Management business names James Morrell as Deputy CEO

Press releases

The newly created Deputy CEO role will provide increased capacity at a senior level to help meet the growing demand for Rothschild & Co’s wealth management services from existing and future clients.

-

Rothschild & Co wins Western Europe's Best Bank for Advisory from Euromoney

Awards

This is the second consecutive year we have been named Western Europe's Best Bank for Advisory, reflecting the breadth of our capabilities across M&A and financing advisory across the region.

-

A mid-year review with our CIO and Global Investment Strategist

Perspectives podcast

A mid-year review on the main macroeconomic developments and how our strategies have perfomed with our CIO Dr. Carlos Mejia and Global Investment Strategist Kevin Gardiner.

-

Global manufacturing revival?

Strategy Blog

As a new manufacturing survey is released in the US, this strategy blog looks at the outlook for the sector and how it could affect the wider economy. Will this lead to an industrial revival across the world? We also assess the impact on Europe and Asia.