The Sick Man of Europe

Trainspotters would have lamented Deutsche Bahn’s fall from grace – dissatisfaction with Germany’s national rail company would give UK train operators a run for their money. Only last year, Swiss transport authorities took the unprecedented decision to ban tardy ‘high speed’ Deutsche Bahn trains from entering the country. While this may be a case of schadenfreude for those of us in less timely nations, for Germany this is no trivial matter and seems emblematic of the strain facing its economy.

Indeed, it’s a been a tough few years for the sick man of Europe, with little respite: Germany’s economy unexpectedly shrank in the second quarter - and is currently little bigger than it was in 2019.

It would be easy to simply conclude that two big negative supply shocks, an overreliance on cheap Russian energy and a global manufacturing downturn have disproportionately affected Germany’s stagnant economy. But is something more fundamental at play?

Cyclical and structural ailment

There is no doubt that consumption and government spending have been subdued in recent years, but at the heart of the apparent malaise lies the German industrial sector - which accounts for perhaps a fifth of output (more than twice that of its European peers). Covid-related disruption and high gas prices have challenged energy-intensive sectors from paint and chemicals through to paper and capital goods.

But not all of Germany’s industrial woes are new – the sector has in fact shrunk every year since 2017 (setting aside a brief covid related bounce in 2020). Today, its industrial economy is one tenth smaller than it was 7 years ago (in contrast, for example, to the US’s which has grown by nearly 4% over the same period). Much of this weakness is linked disproportionately to the auto sector (which accounts for perhaps half of the industrial segment). German car production today, for example, is still one quarter below its average pre-pandemic level. Producers have arguably faced a perfect storm of exogenous and idiosyncratic challenges. From the 2015 ‘dieselgate’ scandal – and associated changes in emission requirements - through to 2018’s trade tensions and even Brexit in 2019 (the UK is an important export market for Germany).

More recently the cost-of-living crisis and the advent of electric vehicles have had an impact too. New cars are exactly the sort of discretionary purchase that nervous consumers will postpone. And traditionally, Germany’s manufacturing expertise lies in the production and assembly of precision components, not in battery manufacturing or software. Internal combustion engines, for example, might have ~200 moving parts, while their electric counterparts have fewer than 20.

Good timing or good planning?

Is Germany simply being left behind, as it were, failing to retool and adapt to changing demands? China, for example, is dominating the EV (electronic vehicle) race, not only displacing Germany globally, but also squeezing its 4th largest export market. Two decades ago, ‘Made in China’ was associated with lower quality manufactured goods, but today it is increasingly able to compete on quality, not just quantity.

The playing field is arguably not entirely level, and some western politicians are eager to protect domestic industry from the glut of EVs – hence there is a range of pending European (and US) tariffs looming for Chinese EV imports. However, there are bigger questions about Germany’s manufacturing and export-driven economic model. Productivity growth has been sluggish and real wages have been rising, and some are beginning to question whether Germany's recent edge was merely a function of fortunate timing.

German competitiveness has long been linked to the success of its Mittelstand, its unique tier of mid-sized, largely bank-financed businesses which accounts for over half of economic output and two-thirds of employment. More recently, efforts to liberalise its labour market in the early noughties, known as the "Hartz reforms", led to significant improvements in labour market productivity, particularly relative to its immediate neighbours. But globalisation – an influx of cheap labour from the former Eastern bloc in the '90s and the outsourcing of supply chains to Asia (China joined the WTO in 2001) – also helped.

It is widely believed that the competitive euro, which replaced a strong D-mark, also played a role, though Germany’s industrial ascent was never primarily about cheapness per se, but about quality (the opposite to that earlier China model).

Macroeconomically, Germany's high savings rate has given it one of the highest current account surpluses in the world (which has recently recovered to ~7% of GDP). This may be good for stability, but hardly leads to a vibrant domestic market.

Political obstacles

Germany’s cyclical outlook may yet improve, if falling interest rates boost weak consumer confidence, and as energy intensive sectors may start to benefit from today’s lower gas prices. However, longer-term aspirations – such as decarbonisation (not easy given its eschewment of nuclear power), a tilt towards a more consumption-led economy and/or a comprehensive retooling of its industrial complex – are all thorny strategic aims that will take time, as well as tremendous political will.

On paper, the government could do more to stimulate growth. There is ample fiscal headroom, reflecting macroeconomic prudence, as net debt-to-GDP stands at a subdued 46% (against the G7 aggregate of 95%). Nor are borrowing costs cause for concern - the longer-dated 10-year bund yield stands at a subdued 2.3%. But Germany’s domestic political difficulties suggest this is unlikely to change.

The current ‘traffic light’ coalition – between the left-wing SPD, the FDP and the Greens – is in a precarious spot. Ambitious plans for economic growth and climate-related spending, co-exist with that tradition of prudence: the longstanding and ongoing obsession with the ‘Schwarze Null’ (black zero), an aversion to government borrowing. The fragmented coalition nearly ruptured late last year, when a constitutional court ruling prevented unused pandemic funds from being redeployed for green initiatives, throwing the budget into disarray. (More recently, the coalition has been weakened further for non-economic reasons, by the reinvigorated AfD at the European Parliamentary elections.)

Investment implications

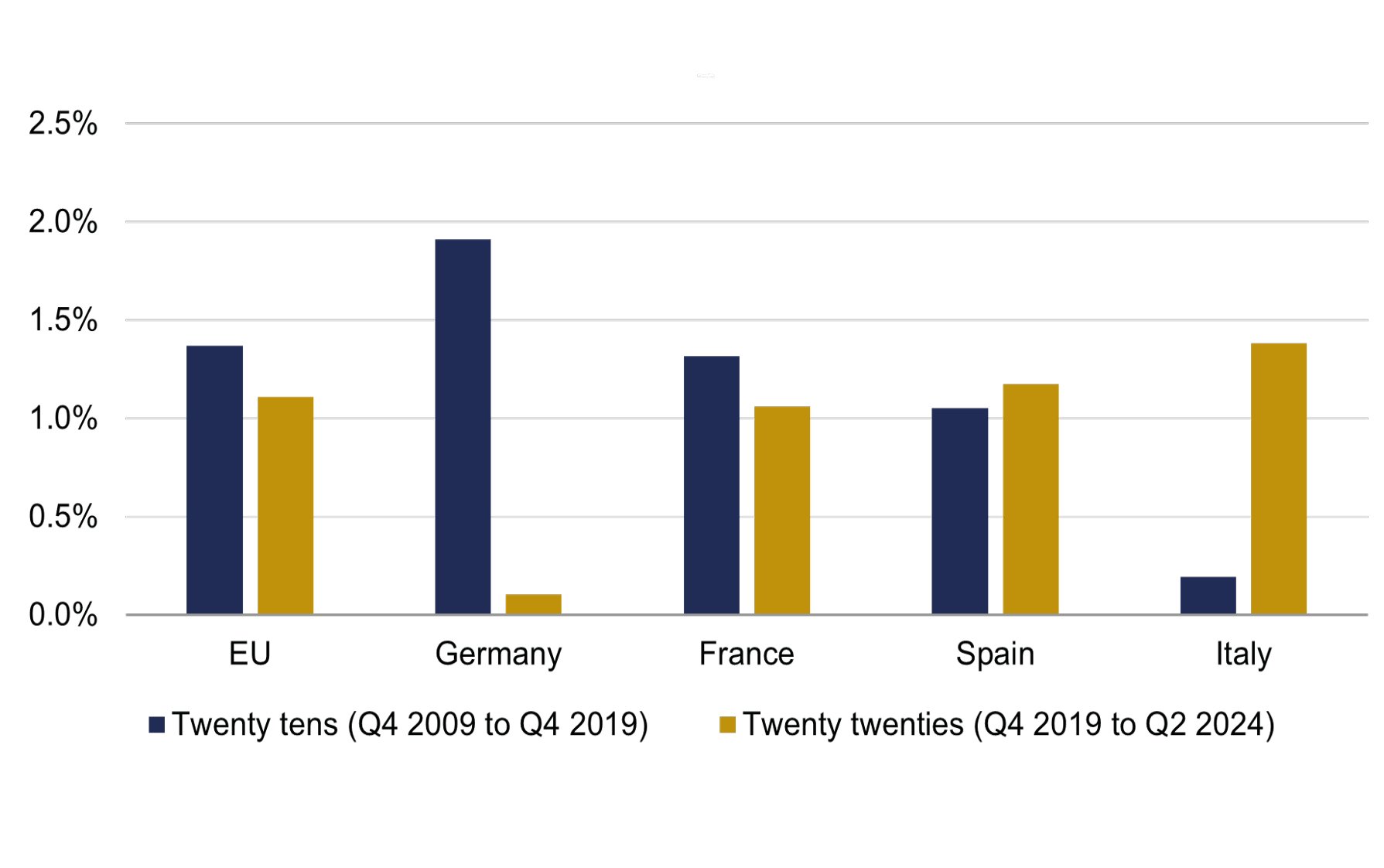

The saying goes that if Germany sneezes, Europe catches a cold – it accounts for nearly a third ($4.5tn) of the bloc’s output. Remarkably, however, the wider bloc has delivered positive output growth in the post covid-years despite Germany’s stagnation – with southern Europe notably picking up the slack.

Eurozone economic output: divergent fortunes

Real GDP (annualised, %)

Source: Rothschild & Co, Bloomberg

Translating these relative national dynamics into actionable investment advice is not straightforward, however. Even as the German economy languishes, the value of many German – and European – listed businesses is often influenced more by global risk appetite and growth than by local concerns. German and European bourses are also not helped by their relative lack of the more exciting technology names which have driven stocks of late.

Perhaps the main conclusion to draw for the time being concerns bonds and interest rates: whatever the cause of Germany’s current woes, while they persist there remains little chance of European rates and yields matching those in the US or the UK.

As for German commuters, it’s not all bad news. Deutsche Bahn is planning reportedly planning a ‘fragrant’ revamp of its rolling stock, while also updating its aging infrastructure. Vorfreude – joyful anticipation – might be a stretch for less patient travellers, but efficiency may yet return. More broadly, we are keeping an open mind about the outlook for the sluggish German economic train.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Read more articles

-

Serious, not hopeless

Market Perspective

Global temperatures are rising. In this Market Perspective we reflect on some of the long-term economic questions raised by climate change. We examine its recent inflationary effect and some of the practical issues we encounter when trying to invest sustainably.

-

Have markets settled down?

Perspectives podcast

Historically, August and September have been weaker months for U.S. stock returns. However, last week’s global market sell-off took investors by surprise. How should we interpret these events, and what do they mean for our strategies?

-

Asset Management: Monthly Macro Insights - August 2024

Market Commentary

Weakening business confidence indices continue to cast doubts on the global economy’s resilience. Although core inflation remains above central banks’ targets, the cooling of labour markets has not gone unnoticed, prompting a major shift in policy rates projections.

-

Growth Equity Update

Insights

The August edition assesses the recent strength of the European VC market. With July also being a strong month for IPOs, with $5.5bn raised in the US. We do a deep dive on LegalTech following a recent spate of VC raises. Plus, we look at the likelihood of the Fed cutting rates in September and the possible market reaction.

-

The AI trade loses some steam

Monthly Market Summary

Global equities moved higher by 1.6% in July (USD terms), while global government bonds returned 1.8% (USD, hedged terms).

-

Rothschild & Co hires Alex Cartel as Managing Director and Head of Global Advisory, Australia

Press releases

In his role, Mr Carter will apply his advisory experience to clients in Australia and bring Rothschild & Co’s global platform to them.