The US labour market: cause for concern?

The monthly US jobs report contains some of the most widely-watched economic indicators in the investment world, but there will be even more attention than usual for this Friday’s release. That’s because the disappointing report from the prior month appeared to be one of the (many) triggers behind the brief bout of market volatility at the start of August. Further unexpected weakness could reignite concerns of a more material US slowdown.

The report comprises of two surveys published by the US Bureau of Labor Statistics (BLS). The first is commonly referred to as the ‘household survey’, and includes the overall unemployment rate (along with other measures related to the labour force). The second is the ‘payrolls survey’, where a large sample of companies – rather than households – are questioned, to produce the closely followed nonfarm payrolls (or jobs) figure.

Employment estimates can diverge between the two surveys due to differences in definitions and estimation methods (fellow ‘macro nerds’ can see the full list here), but as noted, the key figures in both surveys were underwhelming in July. On balance, however, the US labour market still appears to be on the healthier side.

Dissecting the rise in unemployment

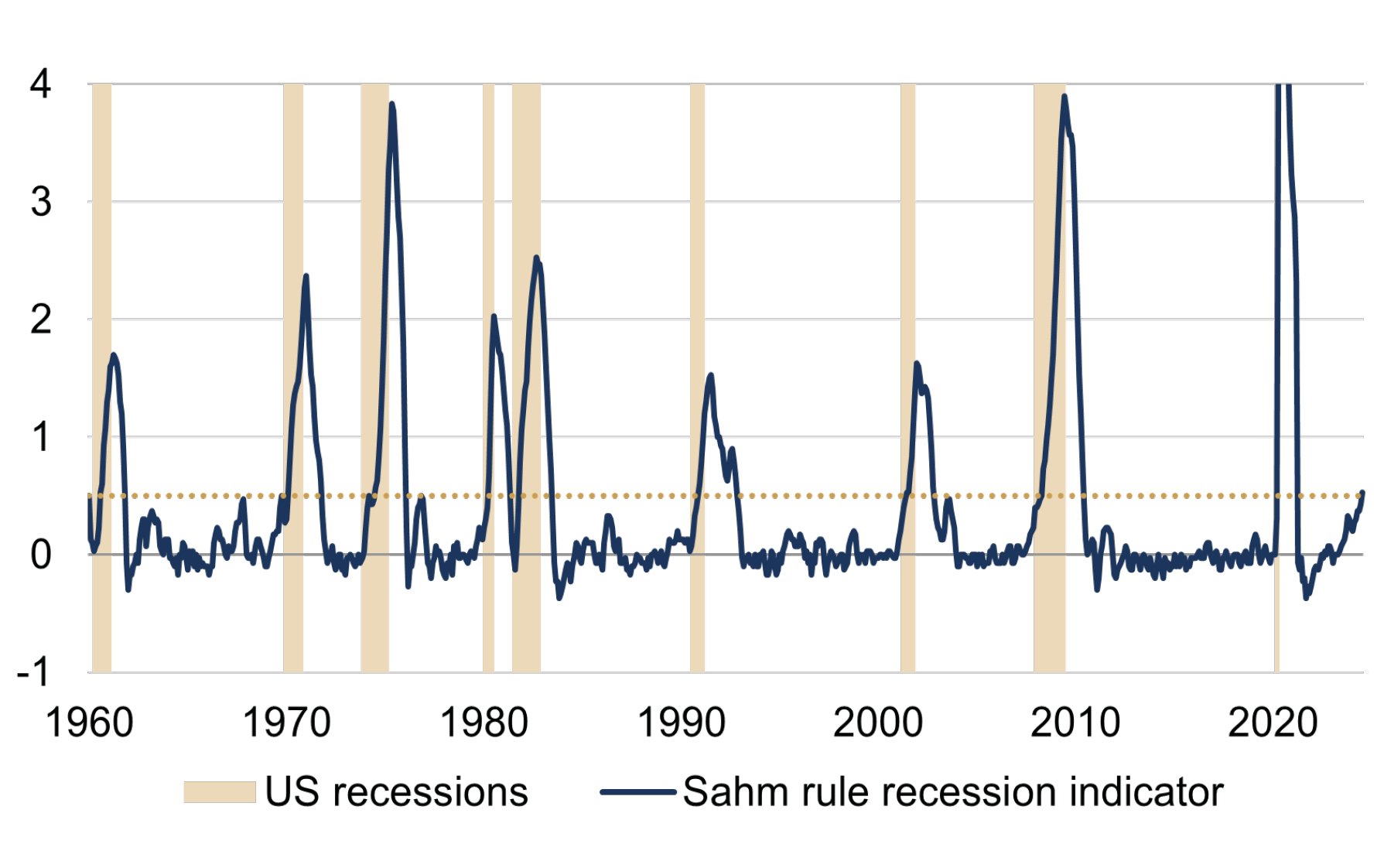

Firstly, in the household survey, the unemployment rate rose to 4.3% in July – its highest reading in almost three years. Recessions tend to occur when the unemployment rate is rising, and pundits have been quick to highlight the so-called Sahm rule as evidence of a looming downturn (figure 1: the rule posits that a recession occurs when the short-term trend in the unemployment rate is at least half a percentage point above its 12-month low). However, the unemployment rate remains low by historical standards – and Claudia Sahm herself, the former Fed economist who identified the correlation, even downplayed it this time around.

Figure 1: Sahm rule recession indicator

Three-month moving average of US unemployment rate (%pts relative to 12-month low)

Source: Rothschild & Co, Bloomberg, NBER, FRED

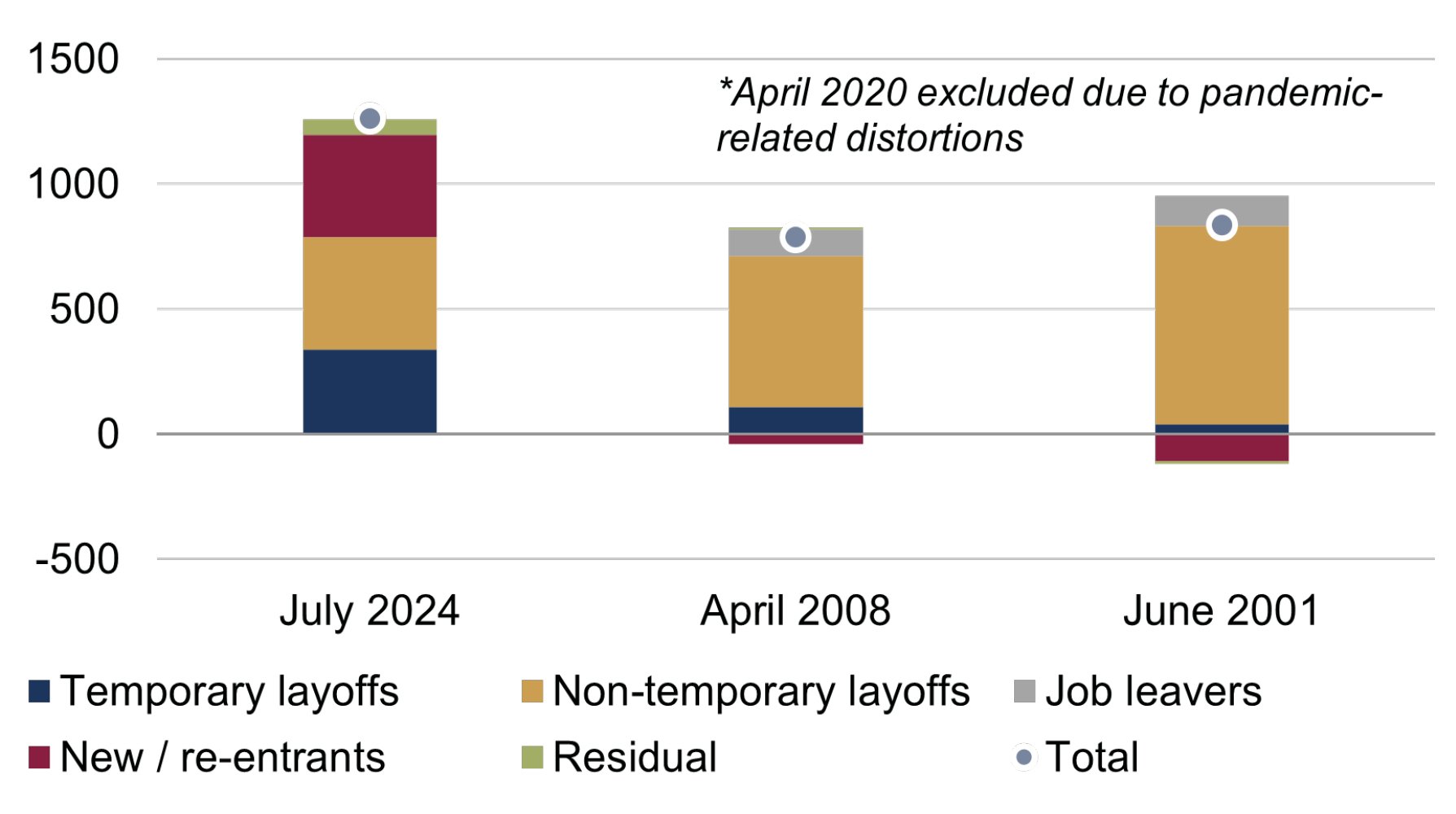

In fact, the underlying drivers of the rise in unemployment suggest a more nuanced picture. The latest rise in US unemployment seems to reflect temporary layoffs to a greater extent than was the case in 2001 and 2008, while non-temporary layoffs (permanent job losers and ‘voluntary’ job leavers) are lower (figure 2). Moreover, the surge in US immigration and the revival of positive real (inflation-adjusted) wage growth rates have led to a large contribution from new entrants and re-entrants to the labour force. Put simply, the rise in unemployment in recent months does not appear to have been caused by firms firing their employees en masse.

Figure 2: Contributions to US unemployment at each Sahm rule trigger

Number of unemployed persons (one-year change)

Source: Rothschild & Co, Bloomberg

Meanwhile, the number of employed persons in the US has only decreased modestly over the past year according to the household survey, again illustrating that the higher unemployment rate has partly been driven by more people entering the labour force. (On a separate note, the relationship between employment and GDP might be expected to vary with changes in productivity trends – and such changes clearly do occur, despite the existence of another questionable ‘rule’ known as Okun’s law).

Payrolls growth in context

Developments in the ‘payrolls survey’ have also been a cause for concern.

After solid nonfarm payrolls growth in the year to March 2024, the US BLS announced a preliminary downward revision of 818,000 jobs for that period – the largest downgrade since 2009. It’s not entirely clear why, though the annual revisions are based on a different – and more comprehensive – sample called the Quarterly Census of Employment and Wages (there has been debate whether the QCEW underestimates the figure due to undercounting undocumented workers), and permanent business closures are incorporated with a lag in the initial dataset. As a result, average monthly jobs growth was downgraded to 174,000 – but this was still roughly in line with its pre-pandemic annual average (2010-19).

Admittedly, nonfarm payrolls have been disappointing in more recent months. In July, only 114,000 jobs were added, meaning growth has averaged 154,000 since March. Again, however, that is only slightly weaker than the pre-pandemic trend. There have in fact been several instances where jobs growth has been much lower – even negative – but that is not the case today. A cooling, rather than collapse, may be the more balanced observation with this survey as well.

Conclusion

Overall, some US labour market slackness has emerged – which is hardly surprising after such a sharp rise in interest rates – but the overall backdrop is not painting a convincing ‘recessionary’ picture. While we cannot rule out further cooling in the labour market, it’s also plausible that its resilience could persist: interest rates are set to move lower from here, and corporate profitability has also turned a corner.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Read more articles

-

Sowing the seeds for regenerative agriculture

Insights

Within 50 years there may not be enough soil left to grow food to feed the world, and more than half of the world’s agricultural land has already degraded. In our third Sustainability Sphere we asked how companies can and individuals address these challenges?

-

The easing cycle commences

Strategy Blog

The Federal Reserve has cut interest rates for the first time since March 2020. The response from markets has generally been positive, but what happens next? In this strategy blog we examine the likelihood of further interest rate cuts in the short term and beyond.

-

Odd one out?

Strategy Blog

Which of the big three Western central banks is most likely to have to reverse their pending rate cuts? In this strategy blog we examine the market expectations form the Fed, European Central Bank and the Bank of England, and outline our own views.

-

Rothschild & Co’s UK Wealth Management business appoints Director of Strategic Relationships

Press releases

Rothschild & Co’s UK Wealth Management business has appointed Daniela Jaume as Director of Strategic Relationships. In this newly created role, Daniela will work closely with the business’s Client Adviser teams to develop relationships and referrals with a network of lawyers, accountants, consultants, and other professional advisers, ensuring clients get the right advice when they need it.

-

Asset Management: Monthly Macro Insights - September 2024

Market Commentary

Global growth is decelerating, but investors expect it will pick up as the impact of monetary policy easing gains traction early next year. Yet, soft landings are hard to track as the early signs of a deceleration look painfully similar to a slide into recession.