Growth Equity Update

June 2024 – Edition 27 – The Artificial Intelligence Edition

- May – Top three European VC raises were for AI businesses. In May, for the first time, the top three European venture capital raises in the month were for AI businesses. The three deals raised $1.6bn with Wayve raising $1.05bn, DeepL $300m and French AI start up H, $220m.

- May – Top three US VC raises were for AI businesses. Also for the first time May saw AI companies take the top three US slots for VC fundraising. Three deals raised $8.1bn. Elon Musk’s xAI raised $6bn at an $18bn valuation. AI cloud infrastructure business CoreWeave raised $1.1bn valuing the company at $19bn. Scale AI, an AI data preparation business, raised $1bn at a $13.8bn valuation.

- ‘The city of lights will become the city of artificial intelligence’. President Macron’s ambition for Paris targets France (and Europe) being the third major AI hub alongside the US and China. Another €400m French government investment programme at nine universities to facilitate AI research is being committed and Microsoft is to invest €4bn to expand its next generation Cloud and AI infrastructure in France. We review similar plans in Germany and Poland.

- Pace of AI investment steps up: In total Europe has seen 22 VC deals in AI ytd to end May raising c$2.3bn versus c$2.9bn for the whole of 2023. We look at where the investment is going.

- Animal spirits: Our Deal Monitor records c$3.4bn of venture raises in Europe in May, up 62% by value on May 2023 and 13% on May 2022. The ytd total is up 44% at $14.8bn. Meanwhile public markets grind higher. AI favourite Nvidia leads the Magnificent Seven up 138% ytd. The S&P World Index is up 11% ytd and IPOs have cautiously resumed on both sides of the Atlantic.

Click here to download a PDF version of Growth Equity Update

Artificial Intelligence - Europe’s ambitions

Ahead of the annual VivaTech conference in Paris at the end of May, President Macron gathered a group of business leaders in Artificial Intelligence at the Elysée Palace. At the previous year’s VivaTech President Macron announced new funding of €500m to ‘create champions’ in AI. Ahead of this year’s VivaTech he announced his ambition that Paris will be the ‘city of AI’ with France (and Europe) being the third major AI hub alongside the US and China.

The city of lights will become the city of artificial intelligence."

Mr Macron announced a new €400m investment programme at nine universities to facilitate AI research sites and to develop relevant talent. He emphasised that training is key and set a target for 40,000-100,000 people a year to be trained in AI techniques. The independent advisory commission, the Conseil National de Numérique will be furnished with a grant of €10m to organise debates and ‘cafés’ around AI in France.

Mr Macron said that ‘for France and Europe, the battle for artificial intelligence is an existential battle, on which our ability to create wealth will depend’ asserting that the AI battle must be fought around ‘ five major areas: talent, infrastructure, uses , investment and governance.’

Speaking at VivaTech former Google CEO Eric Schmidt argued that Europe should invest more in AI and reduce regulation observing that ‘If France doesn’t succeed, Europe will not be a major player in the development of a new form of intelligence, which would be a real tragedy’.

Earlier in May Microsoft announced its largest investment to date in France to accelerate the adoption of AI, skilling and innovation. Microsoft promised ‘€4bn in cloud and AI infrastructure, AI skilling, and French Tech acceleration, aiming to train one million people and support 2,500 AI startups by 2027.’

As part of its €4bn investment to expand its next generation Cloud and AI infrastructure in France, Microsoft will bring 25,000 of the most advanced GPUs to the country by end of 2025. It will expand its datacentre footprint across existing sites in Paris and Marseille and will invest in a new data centre campus in the Grand Est Region, in the Mulhouse Alsace Agglomération.

It plans to help in accelerating AI startups, aiming to engage over 2,500 startups by 2027 with its flagship Microsoft GenAI Studio programme with its package of AI expertise, cloud credits, and support activities. Microsoft GenAI Studio will run a series of 4-month programmes at Xavier Niel’s STATION F, the world’s biggest start up campus in Paris aimed at accelerating the adoption of AI by French startups with technical workshops and access to AI experts at Microsoft and its partners.

Germany has also seen central government initiatives to promote the country as a centre for AI. In August 2023 it announced it would double its funding for artificial intelligence research to €1bn as part of Germany’s Artificial Intelligence Action Plan led by Federal Research Minister Bettina Stark-Watzinger. In December 2023 German start-up Zander Laboratories signed a €30m funding deal with the German government’s cybersecurity innovation agency, the largest single investment by an EU government in AI research.

Germany has also seen substantial investment from Microsoft which in February this year announced plans to invest €3.2bn over the next two years in German artificial intelligence infrastructure. Federal Chancellor Scholz welcomed this ‘empowering investment’. The investment will come over the next two years and will focus on the expansion of Microsoft's cloud region in Frankfurt and newly planned infrastructure in North Rhine-Westphalia. Microsoft will also teach digital skills to more than 1.2 million people in Germany by the end of 2025. Those training programs will focus on AI skills, and will include the first professional certificate for generative AI.

AI in France and elsewhere in Europe has come to the fore in VC fundraises this year. In May, for the first time, the three biggest European raises in a month were for AI with the three deals raising $1.6bn, just under half the monthly total. AI-led UK autonomous vehicle software company Wayve raised $1.05bn; DeepL, raised $300m at a valuation of $2bn. French AI start up H (previously Holistic AI), announced a $220m round.

In total Europe has seen 22 venture capital deals in AI ytd raising around $2.3bn. This compares with an estimated $2.9bn for the whole of 2023. Looking at the largest European AI deals of 2024, all of which have been in May:

AI-led UK autonomous vehicle software company Wayve raised $1.05bn in a Series C led by SoftBank and including Nvidia and Microsoft. It is one of the largest AI raises globally to date. Wayve was founded in London in 2017 and aims to launch the first embodied AI’ technology for self-driving vehicles. Embodied AI allows automated vehicles to learn from and interact with a real-world environment, including the ability to anticipate unexpected and irregular behaviours by other road users. Prime Minister Rishi Sunak said the deal ‘anchors the UK’s position as an AI superpower’.

DeepL, a German/Polish business building an AI powered language platform for translation and writing (it translates texts & full document files instantly) raised $300m at a valuation of $2bn. The round was led by Index Ventures, with participation from ICONIQ Growth and Teachers Ventures as well as existing investors IVP, Atomico and WiL. Founded in 2017 it says its translation technology has ‘a customer network of 100k+ businesses, governments, and other organisations worldwide’ including Zendesk, Nikkei, Coursera and Deutsche Bahn.

Poland has seen substantial government support for the emerging tech scene coordinated by the National Centre for Research and Development. It uses the Polish Development Fund which supports PFR Ventures, a government owned institutional Limited Partner to boost the development of the VC-funded sector. PFR Ventures has an indirect portfolio of over 650 companies. Poland has some 400 R&D centres and has seen investment by big industry names like Google, Microsoft, Amazon, Samsung and Siemens.

French AI start-up H (previously Holistic AI), announced a $220m seed round in May just a few months after the company’s inception. Charles Kantor, the co-founder and CEO, was a university researcher at Stanford and the four other co-founders previously worked for Google’s DeepMind. He was quickly added to the speaker roster at VivaTech after the raise. H intends to develop AI agents, ‘automated systems that perform tasks traditionally undertaken by people.’ Investors include a medley of billionaires, Eric Schmidt, Xavier Niel, Yuri Milner, Bernard Arnault (via Aglaé Ventures) and Motier Ventures (Galeries Lafayette). VC investors include Accel, Bpifrance, Creandum, Elaia Partners, Eurazeo, FirstMark Capital and Visionaries Club. Industrial investors include Amazon and Samsung.

Artificial Intelligence - $2.3bn of raises across 22 deals 2024 ytd

In 2023 Artificial Intelligence deals started to take off in Europe from mid-year and in total there were 34 deals raising $2.9bn. Again governments and state authorities were visibly making an effort to promote a European alternative in the Gen AI world.

The biggest 2023 AI raise was Aleph Alpha’s $500m. The German AI business is producing large language models which allow users to protect data sovereignty. There was a strong Lidl connection with the round led by Innovation Park AI - a foundation established by Dieter Schwarz, the Lidl founder and funded by the state of Baden-Württemberg- and co led by Schwarz Group (the Lidl chain owners) and Bosch Ventures. It is reported that the Aleph founder Jonas Andrulis wanted to raise solely only from European investors.

The leading light of French AI is Mistral AI, set up in May 2023 by a team who had formerly worked at Google and Meta with a plan to launch a LLM by 2024. It is led by Arthur Mensch who has a PhD in machine learning and functional magnetic resonance imaging and who did two years of postdoctoral studies in mathematics before joining Google DeepMind for two-and-a-half years. The company raised €105m ($113m) in a seed round led by Lightspeed in June 2023. It was the largest seed round ever in Europe and valued the four-week-old business at $240m. In early December Mistral closed a new $415m Series A round valuing the company at $2bn, this time led by a16z.

Other AI related raises included Builder.ai’s $250m led by the QIA in May 2023. Builder AI’s Natasha coding platform claims to build automated software apps faster and at considerably lower cost than traditional methods. Previously Microsoft took an undisclosed stake in the business with the aim of integrating the Natasha platform into Microsoft Teams.

Defence AI company Helsing raised $226m in September 2023 in a deal led by General Catalyst which also involved Saab buying a 5% stake for €75m. Helsing was founded in 2021 and describes itself as ‘a new type of defence company, developing AI-based capabilities to protect our democracies.’ It uses AI to process vast amounts of battlefield data to create a decision-making picture. The round valued Helsing at €1.5bn.

UK based Quantexa raised $129m in a Series E valuing the business at $1.8bn in a deal led by Singapore’s GIC and including Warburg Pincus, Dawn Capital, British Patient Capital, Evolution Equity Partners, HSBC, BNY Mellon, ABN AMRO and AlbionVC. Quantexa services banks and other financial institutions using AI and machine learning tools to track and tackle fraud, identity management and compliance issues.

November 2023 saw Israeli Enterprise AI business AI21 raise $208m valuing the business at $1.4bn. Its investors include Intel Capital, Comcast Ventures, Ahren Innovation Capital, Google and NVIDIA. Founded in 2017, AI21 offers advanced large language models and natural language technologies to businesses through application programming interfaces.

Poolside is building an LLM with the aim of enabling users to create code for building applications using plain language. Originally a US company, it raised $26m in May 2023 and followed this up with a $100m round in August led by French entrepreneur Xavier Niel. Simultaneously, the US-founded Poolside decided to move its HQ to Paris.

Artificial Intelligence – 2003 saw $2.9bn of raises across 34 deals

The next chart is drawn from GP Bulldog’s recently published ‘Titans of Technology’ study published in May 2024; view it here.

It breaks Europe’s AI businesses into four categories.

AI in Europe – Four major categories

Data: Data preparation is critical in AI. It is the process whereby raw data is classified, prepared, corrected and tested data for AI model training or to be run through machine learning algorithms.

Europe is represented in this field by three businesses. RavenPack is a Spanish business which reconstitutes unstructured data, primarily for the financial sector ( hedge funds, banks, asset managers). Austrian Mostly.AI is a pioneer in synthetic data generation (real data stripped of personal identifiers) for AI model development. Defined.AI is a Portuguese company building what it calls the largest global marketplace of ethically sourced training data.

Training and tools for AI models, data and infrastructure: Swedish business Kognic is a developer of a software platform to analyse the complex datasets behind advanced driver assistance (ADAS) systems. Run.Ai an Israeli AI workload management business that uses schedulers to help developers optimise their AI hardware infrastructure, was bought in April this year by Nvidia for a reported $700m. It had previously raised $75m in a Series C led by Tiger and Insight in March 2022.

Models. The leading generative AI models are usually closely associated with the major new US Gen AI players developing LLM models. They include OpenAI’s Chat GPT ( valued at c$80bn), Claude by Anthropic (valued at c$15bn) and Elon Musk’s xAI, valued in its recent $6bn raise at $18bn. Cohere, the Canadian start-up which develops large language models for enterprise use has just raised $450m from investors including Nvidia and Salesforce at a valuation of $5bn ( it had $35m ARR in March 2024).

The big tech players are also active in this area. Microsoft has a significant stake in OpenAI and offers its own range of AI tools, the Microsoft Copilot series. In September 2023 Amazon and Anthropic announced a strategic collaboration with Anthropic selecting AWS as its primary cloud provider and agreeing to train and deploy its future foundation models on AWS Trainium and Inferentia chips. In late 2022 Google invested $3bn in Anthropic for a 10% stake with Anthropic sourcing cloud computing capability from Google. In October 2023 Google announced another $500m immediate investment in Anthropic with a further $1.5bn pledged over time. Meta has its own LLM model, Llama 3, released in February 2023.

In Europe Mistral has focused on open source LLMs with its open weight models Mixtral 8x7B and Mixtral 8x22B. Mistral’s most advanced LLM, Mistral Large, is a direct competitor to GPT-4. At present its reputation is of being less functional than GPT-4 but also cheaper.

Hugging Face is a Franco-American US headquartered business founded by three French entrepreneurs. It was a relatively early player in the field launching its first multi-language LLM, BLOOM, in 2022. It last raised in August 2023 with $235m in a Series D led by Salesforce.

AI21Labs of Israel has developed its Jamba base LLM with the capacity to understand and generate natural language.

Stability.AI has focused on its text-to-image generation model, Stable Diffusion but has suffered financial difficulties at the start of 2024, leading to the resignation of CEO Emad Mostaque. Its infrastructure costs (from AWS, Google Cloud Platform and CoreWeave) are reported to have been running at c$100m pa with a further c$55m in staff costs and operating expenses offset by just c$11m pa in revenue. The business last raised $101m in funding led by Coatue in October 2022 and $50m from Intel in the form of a convertible in November 2023.

Applications: This is an area of AI development generating substantial interest, with companies developing applications on the core LLMs designed to address business and consumer needs. The AI models can be fed focused data to train the models into addressing specific sector issues. Combined with applications to fit into existing business processes, this unleashes the potential of AI across businesses, commerce and industry. A range of these niche industry solutions are outlined in the Exhibit. In time, these will go far beyond the customer chatbot, the most commonly cited application for vertical AI software at present.

Europe – The vertical applications of AI – some examples

New European tech unicorns in 2024: Five of the 14 are AI businesses. Of the 14 new unicorns (venture capital-backed companies with a valuation of over $1bn) 2024 ytd, five are AI businesses: -Mistral AI in France, Synthesia.io (software used to create AI generated video content), Builder. AI in the UK, AI21 Labs in Israel and Helsing in Germany.

With Europe’s maturing base of engineering talent and the world’s fascination in its potential productivity gains, artificial intelligence offers a unique opportunity to create global leaders in record time. There is no shortage of funding for the best entrepreneurs and companies…Looking ahead, we expect the next few years to represent an era of unprecedented innovation in the European ecosystem. Innovation is flowing, vast amounts of capital are available for the strong and the talent pool is expanding."

Public markets - grinding higher

Public markets have lost a little momentum in Europe but continue to grind higher in the US. YTD to the 3rd June the Magnificent Seven tech stocks are up 26%, the NASDAQ composite index is up 14%, the tech heavy NASDAQ 100 is up 12% and the S&P 500 is up 11%. The STOXX 600 Europe is up 8%, narrowly outperforming the FTSE 100 +7%. The small-mid caps in the FTSE 250 have started to perform, up 6% ytd with a return of takeover activity.

The Thomson Reuters Venture Capital Index, which seeks to monitor the real time performance of the venture capital industry and whose performance is partly driven by the moves in public markets, and particularly tech heavy indices like NASDAQ, is up 6% ytd but is 11% off its ytd high at the start of March.

Looking at the performance within the Magnificent Seven it is clear that the performance is more narrowly based and that the overall gain is very heavily influenced by the enthusiasm for Nvidia, itself a proxy for the market’s enthusiasm for the potential of AI. In 2023 the Magnificent 7 index was up 75% with performance ranging from the 48% gain at Apple to the 239% rise in NVIDIA.

Ytd in 2024 the basket of stocks is up 26% led by Nvidia at +138% whose market capitalisation has now surpassed that of Apple. This time though Tesla is down 29%, Apple is underperforming broader market indices at +4% and the other four stocks range in the +12% to +38% range.

The Magnificent Seven performance – up 26% ytd with Nvidia the chief contributor

|

2019 - 23 % |

2023 % |

2024 to June 3 % |

|

| Amazon | 102 | 81 | 19 |

| Alphabet | 167 | 58 | 25 |

| Apple | 388 | 48 | 4 |

| Meta Platforms | 170 | 194 | 38 |

| Microsoft | 270 | 57 | 12 |

| NVIDIA | 1383 | 239 | 138 |

| Tesla | 1020 | 102 | -29 |

| Magnificent 7 Index | 271 | 75 | 26 |

Source: Rothschild & Co, Bloomberg

Investor consensus seems to be settling around inflation and interest rate cuts. A ‘ higher for longer’ scenario appears to be priced in and market expectations seem more realistic about the likely pace of interest rate cuts. The US April inflation number, announced in mid-May, was the first one this year to come in lower than expectations at 3.4%, down from 3.5% in March. The Fed’s preferred inflation indicator, the personal consumption expenditure (PCE) index was also in line with expectations, holding at 2.7% in April, the same figure as in March. Core PCE, which excludes food and fuel prices, was 2.8%, in line with expectations.

The next US Fed meeting is on June 12 but there is no expectation in the market of an interest rate cut from the current 23 year high of 5.25%-5.5% at that point. Instead the market expects two 25bps interest rate cuts before the year end with the first one expected in September.

There are still some hawkish views around on interest rates. Neel Kashkari, the Minneapolis Fed president and a Federal Open Market Committee member (albeit without a vote) remarked at the end of May of Americans’ visceral dislike of inflation and commented ‘my best guess is we would leave [rates] here for an extended period of time until we get a lot more data to convince us, one way or the other, is underlying inflation really on its way down.’

European rate cuts have preceded those in the US with the first cut by the ECB happening at its June 6 meeting with a 25bps cut in rates to 3.75% following the 450bps rise between July 2022 and September 2023. Given that the May inflation figure was marginally higher than expectations at 2.6% (April 2.4%) with core inflation at 2.9% it seems likely that an interest rate cut on June 6th may be announced without committing to further future reductions. The market has pencilled in two more interest rate cuts by the end of the year which would take rates down to 3.25%.

The picture in the UK has been muddied by the announcement of an unexpectedly early General Election on July 4. An interest rate cut was not, in any case expected before September after a relatively disappointing April 3.2% inflation figure – forecasters had expected 3.1% while May wage growth of 6% was also higher than expected.

Pace of exits – Subdued, Europe more lively

The IPO window remains open in the US albeit the supply of companies is more trickle than flow. There have been 13 US IPOs raising over $400m ytd (to June 3rd) raising an aggregate total of $10.6bn versus nine IPOs raising over $400m during the whole of 2023, albeit for an aggregate value of $14.1bn.

The performance of the 2024 cohort remains positive. All but one saw a gain on the first day and the weighted day one advance was 17%.

All but one of the 13 IPOs remain in positive territory, with a weighted advance since IPO of 31%.

There is a similar picture in Europe as Q1 2024 saw thirteen IPOs raise €4.8bn (source PWC) - the highest quarterly IPO proceeds since Q1 2021 and some large deals in April and May have brought that total to c$12bn. Of the eight biggest deals ytd in Europe, raising $10.2bn in aggregate, six saw double digit share price advances on the first day of trading and seven were above the placing price at the end of the first week of trading.

The IPO window is open. There is a steady flow rather than a flood of IPOs and sponsors still need to be cautious in terms of investor selectivity and pricing discipline. Nevertheless, the IPO market is building up an attractive record that suggests it is worth the while of investors to participate. Meanwhile, there is little chance of a shortage of supply with, according to Pitchbook data, the backlog of venture-capital-backed firms waiting for an opportunity to go public standing at around 220 companies.

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic:

The favourable mix of growth and disinflation

Venture Capital – AI deals to the fore in May

In a first, the top three deals by value both in the US and Europe in May 2023 were for AI companies

Venture capital raises in Europe remained robust in May 2024. Our Deal Monitor records c$3.4bn of venture raises in the month. This compares with $2.1bn in May 2023 (+62%) and $3.0bn in May 2022 (+13%). It brings the ytd total to $14.8bn, up 44% yoy.

Year to date to the end of May there have been 39 deals raising more than $100m ( 2023 26) plus two deals of $500m and one of $1bn versus zero on both counts to the end of May 2023.

For the first time the top three raises in the month were for AI businesses. The three deals raised $1.6bn, just under half the monthly total with Wayve raising $1.05bn, DeepL $300m and French AI start up H, $220m.

Europe - $3.4bn of VC raises in May – top three raises are in Artificial intelligence

Artificial Intelligence also dominated US raises in May. There were 18 deals raising $100m or more in the month with a total of $11.4bn being raised. The top three were AI deals and raised $8.1bn, 71% of the total.

The largest deal was the $6bn raised by Elon Musk’s xAI which valued the company at $18bn. The business was started in July 2023. In November 2023 it launched Grok-1, an AI LLM 'modeled after the Hitchhiker’s Guide to the Galaxy. It is intended to answer almost anything and, far harder, even suggest what questions to ask!.’ In March Grok-1.5 was launched with improved reasoning capabilities and in its 1.5V version, stronger processing capability for visual information. xAI has also launched an open- source release of Grok-1. The Series B round was supported by investors including Valor Equity Partners, Vy Capital, Andreessen Horowitz, Sequoia Capital, Fidelity Management & Research Company, Prince Alwaleed Bin Talal and Kingdom Holding, amongst others.

Right at the start of May AI cloud infrastructure business CoreWeave raised $1.1bn in a funding round led by Coatue, with participation from Magnetar Capital, Altimeter Capital, FMR, and Lykos Global Management. The round valued the company at $19bn. The previous round from CoreWeave led by Magnetar in May 2023 was for $400m and valued the business at just $2bn. The AI-focused cloud services provider will use the money to service ‘explosive demand for GPU accelerated cloud infrastructure worldwide’. In May CoreWeave opened an office in London as its European headquarters as part of a broader expansion into the continent describing the UK expansion as ‘a £1 bn investment to bolster the country's AI potential.’

Scale AI raised a $1bn Series F led by Accel and Y Combinator valuing the business at $13.8bn. Its previous round was a $325m raise in April 2021 at a valuation of $7.3bn. Scale AI helps companies classify, prepare and test data for AI model training. Its offerings help companies to curate and clean up their data and to build machine learning models trained on that data. In press interviews founder Alex Wang stated that Scale AI’s annual recurring revenue tripled in 2023. The level of ARR was not disclosed although the company targets it to reach $1.4bn by the end of 2024 when the company is also expected to be profitable.

The fourth $1bn raise in May was not in AI but in cybersecurity with four year old US-Israeli business Wiz raising $1bn at a $12bn valuation in a deal led by Andreessen Horowitz, Lightspeed Venture Partners, and Thrive Capital. The cloud security company has indicated that it hit $100m of annual recurring revenue (ARR) after 18 months in existence and reached c$350m in ARR by the end of 2023.

Biggest US VC raises in May ($100m and above) – dominated by AI

The mood of VC investors

It has been a tough couple of years for VC investors with the fall away of the market from its peak in November 2021, the rise in interest rates recalibrating the venture environment, the collapse of Silicon Valley Bank, some spectacular blow-ups like FTX and a much tougher environment in which to raise funds.

The effects of lower returns in VC have taken their toll on fundraising. We know that, according to Pitchbook, global VC fund raising was at just $30.4bn in Q1 putting managers on track to raise just $121bn in 2024, down from of $555bn in 2021 and $188bn in 2023. An April Kaufmann Fellows survey found most VCs expect investors to decrease exposure to the asset class in 2024 with 97% of the 262 respondents believing fundraising will be ‘somewhat to extremely challenging’ in 2024.

Nevertheless our own monitor of fundraises by European VC backed companies indicates that to the end of May the total amount raised ytd was $14.8bn, up 44% yoy, seemingly at odds with the broader caution. Meanwhile the same Kaufmann Fellows survey of 262 of its members managing $250bn, indicated 53% of VC managers surveyed expect to allocate more capital and invest in more startups than last year, with only 6% expecting to invest less.

So is the mood of VC investors improving? The lead indicators would suggest that the mood is lightening amongst VC investors. TCV ( Technology Crossover Venture) has just raised $3bn to target venture investments. In line with other commentators, TCV observes that a better valuation environment in technology and less competition makes VC investing more attractive. John Doran one of TCV’s General Partners on the Executive Committee comments:

“Technology investing is always competitive. That being said, the irrational behaviour we saw really ratchet up in 2021 has gone. We saw hedge funds and venture capitalists try their hand at growth investing and they are largely gone.”

TCV founder Jay Hoag echoes this sense of a more rational and attractive investment environment in VC.

“The world has come our way. In 2021, a hedge fund would have a Zoom call and commit to an India deal in the morning, a China deal at lunch and a US deal in the evening. There was no diligence. That’s gone.”

Speaking at a conference at the start of April Anton Levy, Chairman of the Global Technology Group of General Atlantic observed, in reference to enterprise software and e-commerce that ‘For the first time in a little while, prices…are fair. It’s a great environment to put new capital to work.’

In February 2024 Ibrahim Ajami, Head of Venture at Mubadala Capital was reported in Sifted saying ‘I like to tell my team that we're about four or five quarters into an eight-quarter kind of recalibration. So probably early next year, maybe we'll start seeing things turn around. Could be earlier, could be later.’

By April his optimism appeared to have turned up noting ‘We are moving to offense.’

In early June the European VC investment fund Creandum announced a €500m fundraising which its general partner Carl Fritjossen claimed had been raised ‘in record time’. He commented positively on the state of the industry in the Financial Times.

"There is a dramatic change in the sentiment, appetite and activity across the industry."

Fellow Creandum partner, Sabina Wizander , based in Stockholm commented that:

"From the data we see and from our work every day, we are genuinely very excited about 2024. More quality companies are daring to go out [raising money] because the fundraising environment is more predictable."

Atomico, the tech oriented VC investor, is also indicating a more positive environment for VC investment. Quoted in the FT Tom Wehmeier, the partner who runs its Tech research unit commented:

"We haven’t fully washed through the overhang from the peak years but the green shoots are all around us. We are moving beyond the recovery phase and back into a period of growth."

This optimism is spilling over into the secondary market. New York StepStone Group has just closed a $3.3bn fund to buy stakes in existing VC funds at substantial discounts citing what it calls a ‘massive and growing opportunity’ to buy into attractive assets at depressed prices post the VC boom of 2020-22. Its new fund is 25% bigger than its largest previous fund.

Perhaps some of the growing optimism in VC is based on the enthusiasm for AI as a new potential driver to valuation growth. There appears to be a two tier market in VC in terms of appetite and valuation – artificial intelligence and everything else.

Artificial Intelligence - US Venture Capital raises year to date 2024

Scaling through Chaos

Index Ventures, the tech-focused European VC firm with dual headquarters in London and San Francisco , has produced a guide for founders on how to build their teams. Called ‘Scaling through Chaos’ it bills itself as ‘The Founders Guide to Building and leading teams from 0 to 1000.’

The study has analysed 200,000 career profiles from more than 200 start ups with insights from more than 60 founders. The study is available to read here.

It provides extensive insights into how founders build their teams , what the early priorities are and the likely tenure of staff. We have chosen three charts to highlight.

Potentially there’s not much a founder can do about the first highlight. Turns out that it is best not to start your company alone. According to the Index Ventures survey the majority of successful start-ups have two or more founders. 71% of the successful companies have two or three founders. Just 12% of successful companies have a solo founder.

Lone founders may be consoled by discovering that the successful amongst them are, however, in the company of Amazon’s Jeff Bezos, Craigslist’s Craig Newmark and SpaceX’s Elon Musk.

The next chart highlights Index’s assertion that once they have developed a minimum viable product and have initial venture funding company, founders spend a substantial part of their time dealing with people and hiring. The Index Ventures finding is that half of founders’ time is spent on people related issues.

Our third selected chart relates to the hiring priorities of early stage companies. The chart looks at the commonest executive role hires as a start up gets to 50 people. The advice from Index is not to overload with executive hires at an early stage, both because the business will likely not be able to afford it and because the calibre of the candidates is unlikely to be what the business will want in the longer term. Perhaps not surprisingly, General Manager is the favoured choice of early stage start-ups followed by CTO and COO.

It is always a surprise to see how low in these lists the role of Chief Financial Officer comes – just 14% of the companies of 50 people or so have one. This though is perhaps a function of what Index Ventures calls ‘fractional executives’ - operators who spread their time across a number of startups during the period before a full-time executive is hired into the role.

Our views on the state of the venture capital markets

2022 saw sharp falls in the public markets on the back of a combination of global inflation, rising interest rates, and increased geopolitical risk. In 2023 there was a substantial rally on NASDAQ, led by the major tech stocks, a rally more palely reflected in other markets. The Refinitiv Venture Capital Index, which seeks to monitor the real time performance of the venture capital industry, fell 55% in 2022. In 2023 it was up 56%. YTD in 2024 it is up 6% meaning the total fall since the peak at end November 2021 is 34%. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment has had a sharp impact on valuations in private markets. The scale of the fall in the Refinitiv VC index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023

- There is substantial dry powder in the VC industry. This though appears to be prioritised to support existing rather than new investments

- Best-in-class companies, addressing critical rather than nice-to-have requirements, continue to attract support. There are still hotspots for investment most notably in Artificial Intelligence and Climate Tech. Certain investors remain very active in the space with substantial funds to deploy

- The speed of the investment process has slowed considerably. The level of diligence on new deals has stepped up

- For much of 2023 big late-stage deals were few and far between with the strongest part of the market in terms of appetite being in Seed and Series A where there is less immediate pressure on valuation. The last few months though have seen a notable pick-up in large deals, particularly in AI and Climate Tech

- 2023 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these. These continue into 2024.

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses

- Valuation priorities have shifted with investors having moved away from an emphasis on revenue growth and revenue multiples. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and an emphasis on DCF and comparative based multiples.

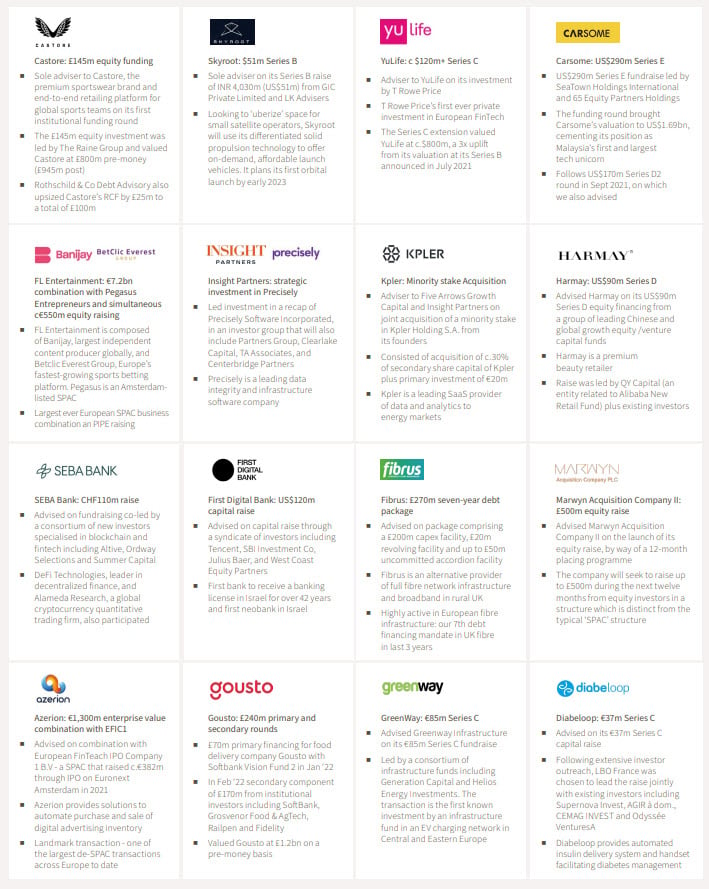

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Mark Connelly

Head of North American Equity Market Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

Stéphanie Arnaud

Managing Director – France

stephanie.arnaud@rothschildandco.com

+33 1 40 74 72 93

+33 6 45 01 72 96

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023 , December 2023 , January 2024, February 2024, March 2024, May 2024

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.

Read more articles

-

Macro update: polls, populists, policy and portfolios

Strategy Blog

In this strategy blog, we look at how polls, populists, policies and portfolios are affected by recent, and upcoming macro events.

-

Our culture, service and people

Insights

We pride ourselves on our company culture, values and people at Rothschild & Co Wealth Management UK. Our business is built on the strength of our people and the relationships they have with clients, and we believe this sets us apart from other wealth managers.

-

Sportonomics and the winners away from the arena

Thematic Insights

The Olympic motto 'citius, altius, fortius' - faster, higher, stronger - reflects the sport industry's rapid evolution. Younger generations are redefining their engagement with athletes and sports, driven by new technologies.

-

Making the best investment choices

Insights

There are many ways you can grow and preserve your wealth by investing. In this article we discuss how to find an investment style that suits your outlook, examine both ‘top-down’ or ‘bottom-up’ investing strategies, and assess active and passive investing.

-

How to choose a wealth manager

Insights

Wealth can be easily lost if you are not prudent. A wealth manager can help you avoid this fate, but you need to be confident that you're making the right choice. In this article we outline the key questions to ask and how they can hep you meet your financial goals.