Few US stocks drive global markets

Investment Communications Team, Investment Strategy Team, Wealth Management

Summary

Global equities rose by 2.2% in June (USD terms), while global government bonds returned 0.9% (USD, hedged terms). Key themes included:

- Stock markets rose further, mostly led by the US mega-cap names;

- The ECB commenced its easing cycle. The Fed is expected to follow this year;

- European politics moved into focus with Macron’s snap election decision.

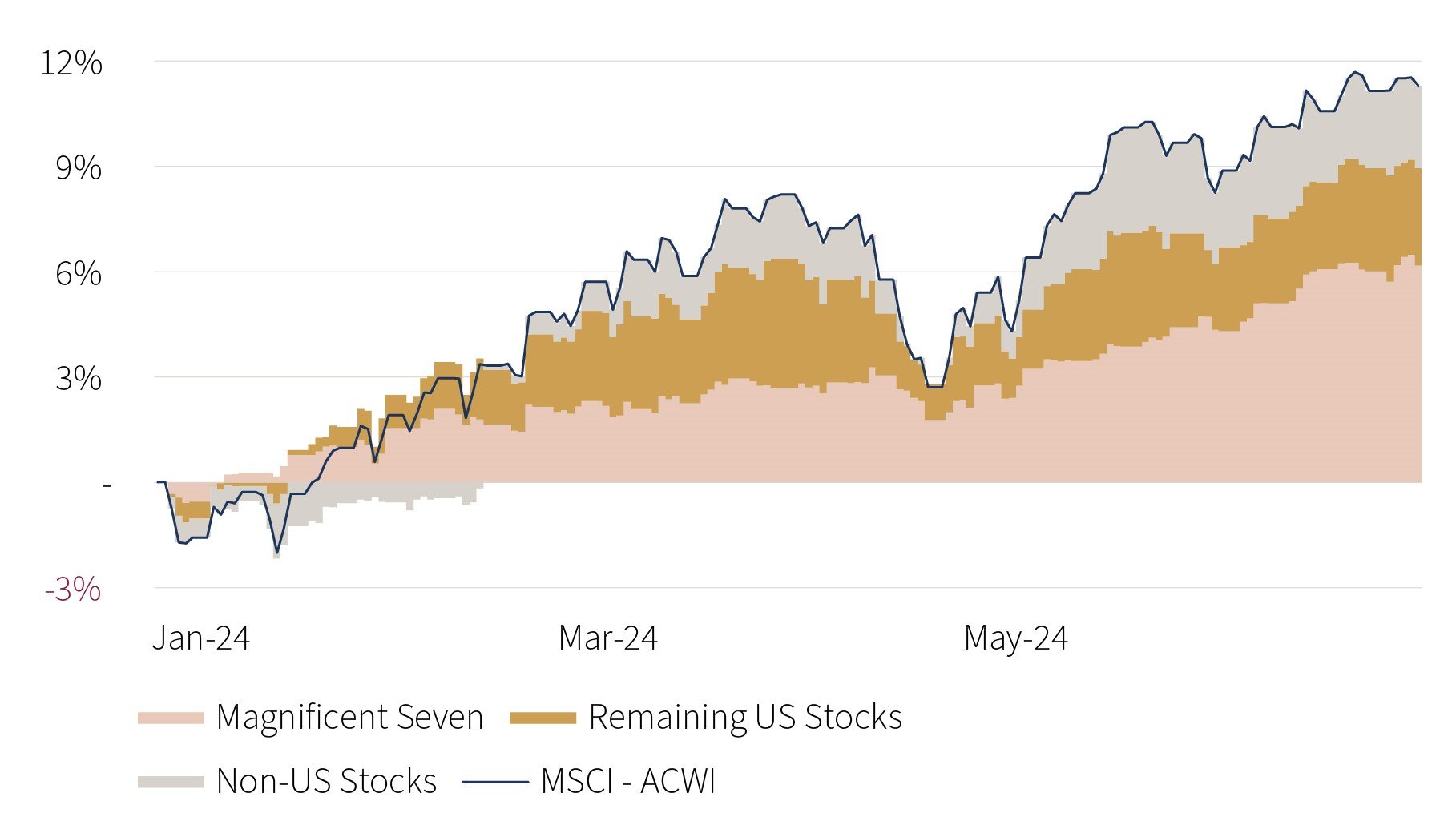

Global stock market contribution - Year-to-date (%pts, USD)

Source: Rothschild & Co, Bloomberg

Chart note: The Magnificent Seven consist of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Markets: A narrow stock market ascent

Global stocks rose to fresh highs in June, though this was again largely driven by the US market – and within it, some of its (AI-related) mega-cap names. Global stocks excluding the US were flat in June, as was the equal-weighted US index. The EM Asia cohort also stood out, with the two big semiconductor-intensive nations – Taiwan and Korea – outperforming. In fixed income, 10-year government bond yields modestly drifted lower across the US and Europe – a prominent exception being France, where the OAT spread over Germany widened after Macron’s surprise snap election decision (however, the spread remained tighter than during the eurozone debt crisis). In currency markets, the euro softened against most major currencies, yet it was the Japanese yen which stood out: it weakened to multi-decade lows against the US dollar and to a record low against the euro. Commodity prices fell in June – particularly industrial metals and agriculture – but Brent Crude oil rebounded by 6%, to $86 p/b.

Economy: Inflation patchily abating

Real-time US GDP estimates continued to suggest another quarter of solid economic growth, with retail sales and industrial production expanding in May, though the closely-watched ISM manufacturing PMI remained subdued in June. The labour market also remained tight and jobs growth in May surpassed economists’ expectations. US inflation continued to cool: the headline rate edged lower to 3.3% (y/y), while core inflation fell to 3.4% – its lowest reading in three years. In Europe, the timelier business surveys softened in June, but continued to signal economic expansion. UK hard data remained robust: monthly GDP stagnated in April, but this was ahead of consensus, and May retail sales rebounded strongly. Inflation developments were mixed. Eurozone inflation moved higher in May, though both the headline and core rate remained below 3%. Services inflation reaccelerated, and remained the stickiest CPI category on both sides of the Atlantic. Promisingly, UK headline inflation fell to the Bank of England’s 2% target, while core inflation moved lower as well, albeit to a higher rate of 3.5%.

Policy: ECB and SNB cut rates; Macron’s gambit?

Several developed-market central banks began their easing cycles in June. Among those, the European Central Bank unsurprisingly cut its deposit rate by 25bps, to 3.75%, while the Swiss National Bank lowered its main policy rate for the second consecutive meeting. Conversely, the US Federal Reserve and Bank of England left their interest rates unaltered – but both suggested that they were still likely to move lower this year. The former’s updated interest rate projections were more hawkish, showing just one cut in 2024. Meanwhile, the Bank of Japan’s ultra-loose policy stance was unchanged.

It was a busy month within the election cycle: the first US presidential debate took place – which featured a concerning performance from Biden – and incumbent parties retained power in India, Mexico and South Africa. In the European Parliamentary election, there was a shift to the right, with the centre-right EPP – and far-right parties – gaining seats at the expense of the centre-left and green parties. However, the major surprise was Macron’s decision to call a snap parliamentary election in France, in which Le Pen’s Rassemblement National gained a third of votes in the first round (Macron’s alliance obtained just over 20% of the vote). Elsewhere, the UK was set for its general election on July 4th, with Labour remaining well ahead in the polls.

Performance figures (as of 28/06/2024 in local currency)

| Equity (MSCI indices $) | Month | Year |

|---|---|---|

| Global | 2.2% | 11.3% |

| US | 3.5% | 14.6% |

| Eurozone | -2.9% | 6.4% |

| UK | -1.8% | 6.9% |

| Switzerland | 0.0% | 1.8% |

| Japan | -0.7% | 6.3% |

| Pacific ex Japan | 0.3% | 0.7% |

| EM Asia | 5.0% | 11.0% |

| EM ex Asia | -0.1% | -5.1% |

| Fixed income | Yield | Month | Year |

|---|---|---|---|

| Global Govt (hdg $) | 3.36% | 0.9% | -0.1% |

| Global IG (hdg $) | 5.04% | 0.7% | 0.3% |

| Global HY (hdg $) | 8.26% | 0.7% | 3.9% |

| US 10Y | 4.40% | 1.3% | -1.6% |

| German 10Y | 2.50% | 1.5% | -2.4% |

| UK 10Y | 4.17% | 1.3% | -2.6% |

| Switzerland 10Y | 0.60% | 2.7% | 1.4% |

| Currencies (NEERs) | Month | Year |

|---|---|---|

| US Dollar | 1.7% | 4.7% |

| Euro | -0.7% | 0.4% |

| Pound Sterling | 0.2% | 2.9% |

| Swiss Franc | 1.6% | -3.4% |

Table note: NEERs under ‘currencies’ are the JP Morgan trade-weighted nominal effective exchange rates

| Commodities ($) | Level | Month | Year |

|---|---|---|---|

| Gold | 2327 | 0.0% | 12.8% |

| Brent Crude oil | 86 | 5.9% | 12.2% |

| Natural gas (€) | 34 | 0.8% | 6.6% |

Source: Bloomberg, Rothschild & Co.

Read more articles

-

Is a wealth manager worth it?

Insights

We all like to achieve good value for money, but it's particularly important when choosing a wealth manager. You are entrusting someone with you and your family’s financial future, and in this article we outline how to assess the value of a wealth manager.

-

Five stock market talking points

Strategy Blog

Stocks have continued their ascent during the first half of this year, with the global benchmark up 11% in US dollar terms. As we reach the halfway point in the year, we examine the performance of global stock markets and outline five key things we’ve learnt so far in 2024.

-

French election: first-round outcome

Strategy Blog

In this strategy blog, we look at the first-round of the French election, and how local markets could be affected by the final verdict.

-

Macro update: polls, populists, policy and portfolios

Strategy Blog

In this strategy blog, we look at how polls, populists, policies and portfolios are affected by recent, and upcoming macro events.

-

Our culture, service and people

Insights

We pride ourselves on our company culture, values and people at Rothschild & Co Wealth Management UK. Our business is built on the strength of our people and the relationships they have with clients, and we believe this sets us apart from other wealth managers.