32 / 204

32 / 204

30

Rothschild & Co | Annual Report 2017

2013

2015

2014

2017

(1)

2016

41.2

44%

56%

43% 47.8

57%

51.0

40%

60%

54.0

59%

41%

63%

37%

67.3

Asset Management

Private Wealth

0.7

1.0

-0.3

1.0 3.4

2.4

2.6 0.3

2.3

1.2

0.3 0.9

1.3 0.4

1.7

Asset Management

Private Wealth

2013/14

(12m to Mar)

2014/15

(12m to Mar)

2015/16

(12m to Mar)

2016/17

(12m to Mar)

(1)

2017

(12m to Dec)

(1)

.

.

-

.

.

.

.

.

.

.

.

.

.

.

.

.

Asset anage ent

Private ealth

2013/14

(12m to Mar)

2014/15

(12m to Mar)

2015/16

(12m to Mar)

2016/17

(12m to Mar)

(1)

2017

(12 to Dec)

(1)

Rothschild Private Wealth & Asset Management

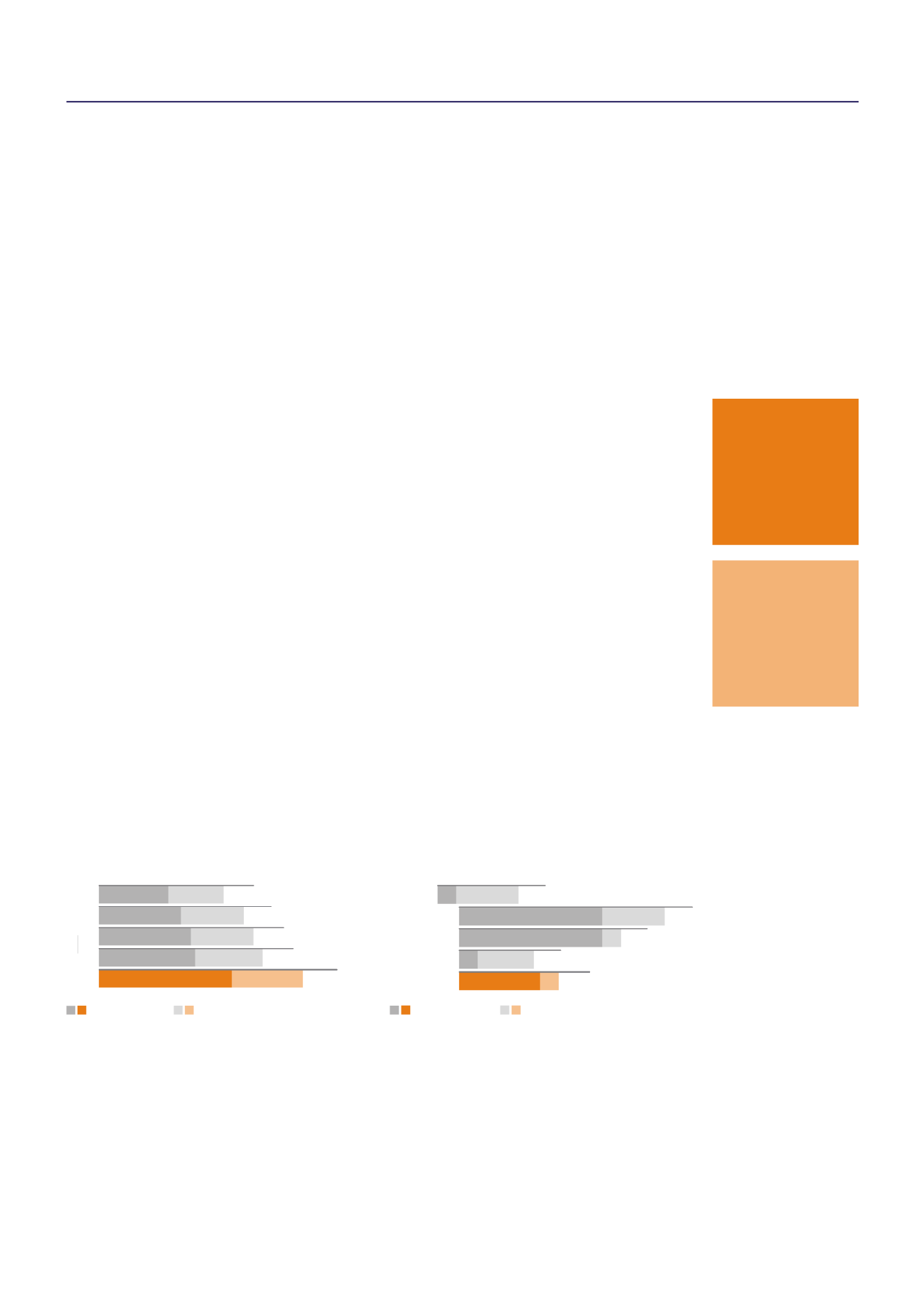

€67.3bn

of Assets under

management as

at 31 December

2017

€1.7bn

of net new assets

in 2017

We serve a diverse client base from our offices in Aix-en-Provence, Brussels, Frankfurt, Geneva, Grenoble, Guernsey, Hong

Kong, London, Manchester, Marseille, Milan, Monaco, New York, Paris, Reno, Singapore and Zurich.

We continue to develop our activities in line with our stated strategy of diversifying our sources of income.

Market overview

Investment markets remained broadly benign through 2017.

Global stock markets comfortably outpaced most inflation

rates, and did so with unusually low levels of volatility. Bonds

lagged behind stocks, but most corporate bonds at least also

managed to beat inflation.

The economic expansion gathered some momentum and

broadened into one of the most widely-based upturns seen

in recent years. The developed world grew at a respectable

pace, with the Eurozone in particular continuing to outpace

expectations, while China’s economy defied sceptics

to deliver neither a hard nor soft landing but a small

acceleration. Unemployment dropped to multi-decade lows

in the US, UK, Germany and Japan, while corporate profits

growth resumed after the interruption caused by falling oil

and mining profits in 2015/2016.

The year had started with political concerns uppermost in

many investors’ minds. In the event, the US administration’s

protectionist talk did not translate into action, and the year

ended with the passage of significant tax-cutting measures

that seem set to boost US growth and corporate profits

further. In Europe, talk of a populist backlash against the EU

proved premature: the year ended with President Macron

embarked on a programme of liberal reform in France,

and Chancellor Merkel seemingly poised to form another

administration in Germany. Negotiations over UK secession

from the EU proved less disruptive than feared, but the

snap election in mid-year left it, alone amongst the major

countries, facing increased political uncertainty at year end.

There remain few signs of economic excess in this

increasingly lengthy business cycle. However, market

valuations are relatively full, and monetary conditions may

start to normalise a little faster. A long-overdue revival in

volatility seems to have started in February. Nonetheless,

the next financial year begins at least with the economic

climate a broadly constructive one.

Rothschild Private Wealth offers an objective long-term perspective on investing,

structuring and safeguarding assets, to preserve and grow our clients’ wealth.

Rothschild Asset Management offers an independent perspective in innovative

investment solutions, designed around the needs of each and every client.

Net new assets

(in billions of euros)

Assets under management

(in billions of euros, as at 31 December)

(1) Including Martin Maurel Group.