142 / 204

142 / 204

140

Rothschild & Co | Annual Report 2017

Rothschild Bank International Limited

RBI complies with the liquidity regime of the GFSC. Historically, the GFSC prescribed cumulative cash flow deficit limits for periods up to the one-month time

horizon using standard behavioural adjustments (i.e. not institution specific).

At 31 March 2017, the RBI regulatory liquidity ratio for the eight-day to one-month period as a percentage of total deposits was 18.1%, well in excess of the

limit set by the GFSC of -5%.

The GFSC amended the minimum regulatory liquidity requirements that apply to licensed deposit takers incorporated in Guernsey with effect from 31 July

2017. RBI’s LCR under the new requirements at 31 December 2017 was 186%. The regulatory limit is 100%.

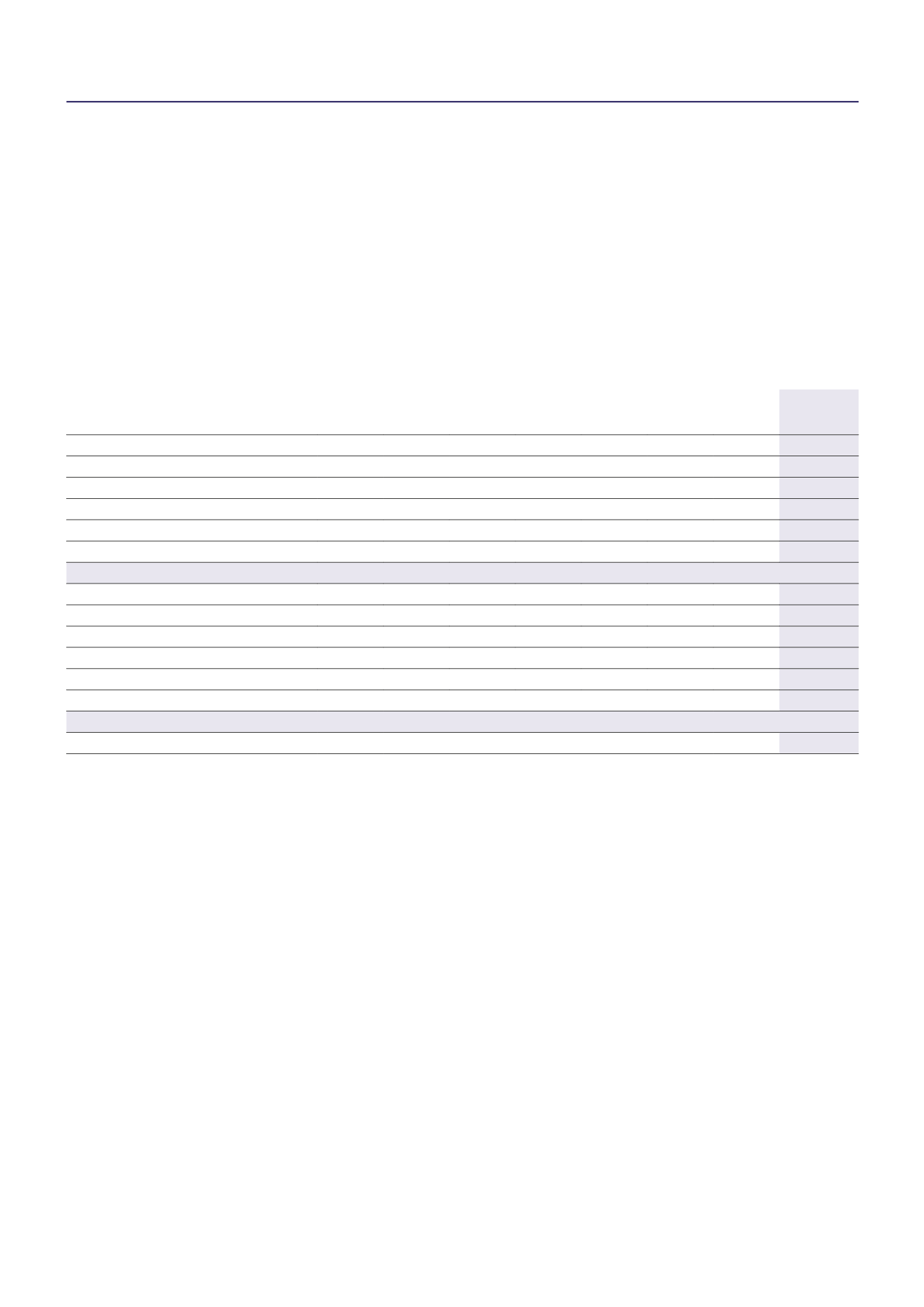

2 Contractual maturity

The following table shows the Group’s financial assets and liabilities, analysed by remaining contractual maturity at the balance sheet date.

In millions of euro

Demand-

1m

1m-3m 3m-1yr

1yr-2yr

2yr-5yr

>5 yr

No

contractual

maturity

31/12/2017

Cash and balances at central banks

3,868.9

–

–

–

–

–

– 3,868.9

Financial assets at FVTPL

15.0

1.2

3.6

0.8 215.0 164.3 148.1

548.0

AFS financial assets

552.3 113.1 321.9 234.9 134.6

50.9 188.6 1,596.3

Loans and advances to banks

1,542.6 167.6

20.0

–

–

–

–

1,730.2

Loans and advances to customers

718.5 485.0 713.5 418.2 398.1 256.6

– 2,989.9

Other financial assets

395.0

29.4

1.8

0.1

0.1

–

–

426.4

TOTAL

7,092.3 796.3 1,060.8 654.0 747.8 471.8 336.7 11,159.7

Financial liabilities at FVTPL

20.5

3.2

1.1

–

–

–

–

24.8

Hedging derivatives

–

–

–

–

6.5

–

–

6.5

Due to banks and other financial institutions

284.5

50.2

5.9

16.5 115.9 163.4

–

636.4

Due to customers

7,571.5

70.8

86.5

25.0

16.7

0.5

–

7,771.0

Debt securities in issue

0.1

50.6

43.4

1.5

–

–

–

95.6

Other financial liabilities

146.6

2.7

0.8

–

–

–

–

150.1

TOTAL

8,023.2 177.5 137.7

43.0 139.1 163.9

– 8,684.4

Loan and guarantee commitments given

358.0

15.5

65.8

11.3 105.5

7.7

–

563.8

Loan and guarantee commitments given are disclosed in the period in which they could first be drawn down.

The undiscounted cash flows of liabilities and commitments are not materially different from the amounts disclosed in the contractual maturity table above.

E. Fair value disclosures

1 Fair value classification

For financial reporting purposes, IFRS 13 requires fair value measurements applied to financial instruments to be allocated to one of three levels, reflecting

the extent to which the valuation is based on observable data.

Level 1: instruments quoted on an active market

Level 1 comprises instruments whose fair value is determined based on directly usable prices quoted on active markets. This mainly includes listed securities

and derivatives traded on organised markets (futures, options, etc.) whose liquidity can be demonstrated, and shares of funds where the value is determined

and reported on a daily basis.

Level 2: instruments measured on the basis of recognised valuation models using observable inputs other than quoted prices

Level 2 comprises instruments not directly quoted on an active market, measured using a valuation technique which incorporates parameters that are

either directly observable or indirectly observable through to maturity.

Notes to the consolidated financial statements